IFT Notes for Level I CFA® Program

LM01 Derivative Instrument and Derivative Market Features

Part 1

1. Introduction

Cash markets refers to markets in which financial assets like equities, fixed income securities, currencies and commodities are exchanged at current prices. Cash markets are also known as spot markets because the transactions are settled on the spot.

In contrast, derivatives involve the future exchange of cash flows whose value is derived from or based on an underlying value.

This learning module covers what is a derivative, the different types of derivatives, and the basic features of a derivatives market.

2. Derivative Features

Definition and Features of a Derivative

A derivative is a financial instrument that derives its value from the performance of an underlying asset. In simple terms, a derivative is a legal contract between a buyer and a seller, entered into today, regarding a transaction that will be fulfilled at a specified time in the future. This legal contract is based on an underlying asset.

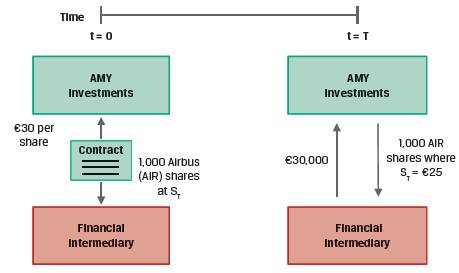

For example, exhibit 1 from the curriculum shows a ‘forward contract’ which is a type of derivative.

In this example:

- AMY Investments agrees today (t = 0) to deliver 1,000 shares of Airbus (AIR) at a fixed price of €30 per share on a future date (t = T), which in the example is six months.

- The forward contract allows AMY to transfer the price risk of the underlying to the counterparty.

- If the spot price of AIR is €25 after six months, AMY will still receive €30,000 from the counterparty in exchange for 1,000 AIR shares (which are now worth just €25,000). Alternatively, AMY could simply settle with the intermediary the €5,000 difference in cash.

A derivative contract is a legal agreement between counterparties that defines the rights of each party involved. There are two parties participating in the contract: a buyer and a seller.

- Long: Buyer of the derivative is said to be long on the position. He has the right to buy the underlying according to the conditions mentioned in the contract.

- Short: Seller of the derivative is said to be short. Remember “s” is for short and seller.

A stand-alone derivative is a distinct derivative contract such as a derivative on a stock or bond. In contrast, an embedded derivative is a derivative within an underlying, such as a callable, puttable, or convertible bond.

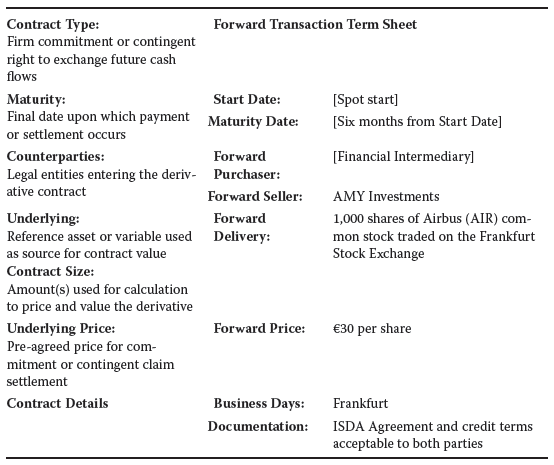

Exhibit 2 from the curriculum provides a sample forward contract term sheet for the AMY example.

Derivatives can be divided into two types:

- Firm commitments: Both long and short parties have an obligation to complete the transaction. Example: forwards, futures, swaps

- Contingent claims: Seller has the obligation. The buyer has a right but no obligation to complete the transaction. Example: Options, credit derivatives.

Derivative markets expand the set of opportunities available to market participants beyond the cash market to create or modify exposure to an underlying. For example,

- Investors can sell short to profit from a decline in the underlying’s value.

- Investors can use derivatives to diversify their portfolios.

- Investors can offset financial market exposure associated with a commercial transaction.

- Investors can create large exposures to an underlying with a relatively small cash outlay.

- Derivatives are typically more liquid and have lower transaction costs than the underlying.

Investors can use derivatives for hedging. This involves offsetting or neutralizing an existing or anticipated exposure to an underlying.

3. Derivative Underlyings

The most common derivative underlyings include equities, fixed income and interest rates, currencies, commodities, and credit.

Equities

- Equity derivatives can be based on an individual stock, a group of stocks, or a stock index.

- Options on individual stocks are often used by companies as compensation for their employees. Options encourage employees to work to increase the equity value of the company.

- Index swaps, also known as equity swaps, allow investors to pay the return on one stock index in exchange for the return on another index or interest rate.

- Derivatives are also available based upon the realized volatility of equity index prices over a certain period. This allows investors to manage the magnitude of price changes separately from the direction of the change.

Fixed-Income Instruments

- Derivatives based on bonds are widely used. Since government issuers have many similar bond issues outstanding, bond futures typically allow more than one bond issue to be delivered to settle the contract.

- Derivatives based on interest rates are also common. Here the underlying is not an asset.

- Interest rate swaps can be used to convert from a fixed to a floating interest rate exposure over a certain period. A market reference rate (MRR) is the most common interest rate underlying used in interest rate swaps. These rates are based on a daily average of observed market transactions, e.g., the Secured Overnight Financing Rate (SOFR) is an overnight cash borrowing rate collateralized by US Treasuries.

Currencies

- Currency derivatives are often used to hedge the exposure of commercial (e.g. exporters and importers) and financial transactions (e.g. an investor holding foreign securities) that arise due to foreign exchange risk.

Commodities

- Commodities can be classified into soft commodities (agricultural products such as cattle and corn) and hard commodities (natural resources such as crude oil and metals).

- Commodity derivatives are often used to hedge the price risk of commodities. For example, an airline may purchase oil futures to hedge against higher fuel costs in the future.

Credit

- Credit derivatives are based on the default risk of a single issuer or a group of issuers in an index.

- Credit default swaps (CDS) allow an investor to manage the risk of loss from borrower default separately from the bond market.

Other

- Derivatives can also be based on several different types of underlying such as weather, cryptocurrencies, longevity etc.

4. Derivative Markets

In this section, we look at the characteristics of over-the-counter (OTC) and exchange-traded derivatives (ETD) markets.

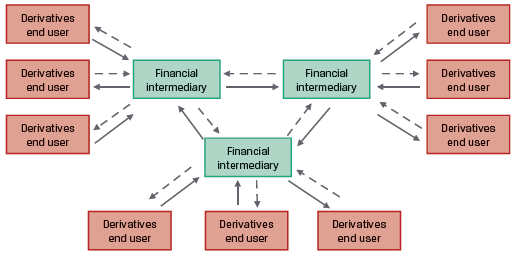

Over-the-Counter (OTC) Derivative Markets

- OTC derivatives market involve contracts between derivatives end users and dealers (financial intermediaries such as commercial banks and investment banks).

- The terms of the contracts can be customized as per the end user’ needs. This flexibility is important to end users seeking to hedge a specific exposure based on non-standard terms.

- OTC dealers, also called market makers, typically enter into offsetting transactions with one another to transfer risk to other parties.

- OTC instruments have less transparency and more counterparty risk as compared to ETD.

- Exhibit 4 from the curriculum illustrates the structure of an OTC derivatives market.

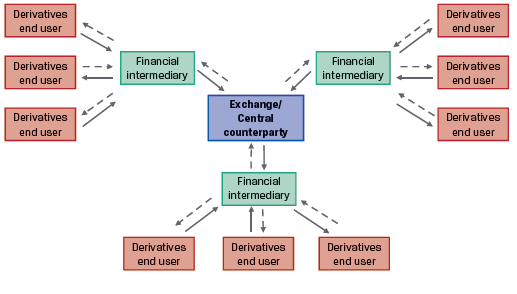

Exchange-Traded Derivative (ETD) Markets

- Exchange-traded derivatives are standardized. The terms and conditions—such as the size of each contract, type, quality, and location of underlying for commodities and maturity date—are set by the exchange. There is no room for customization.

- Standardization leads to a more liquid and transparent market.

- Standardization also facilitates an efficient clearing and settlement process. Clearing is the exchange’s process of verifying the execution of a transaction, exchange of payments, and recording the participants. Settlement involves the payment of final amounts and/or delivery of securities or physical commodities between the counterparties.

- To provide a guarantee against counterparty default, derivative exchanges require both the long and short party to post collateral when a trade is initiated. Additional collateral may be required based on the price movements of the underlying during the life of the trade.

- ETD markets are transparent – full information on all transactions is disclosed to the exchanges and national regulators.

- Exhibit 6 from the curriculum illustrates the structure of ETD markets.

Central Clearing

- After the 2008 global financial crisis, global regulatory authorities instituted a central clearing mandate for most OTC derivatives. This mandate requires that a central counterparty (CCP) assume the credit risk between derivative counterparties. The CCP provides clearing and settlement.

- End users have the flexibility to customize contracts when facing financial intermediaries. While the management of credit risk, clearing, and settlement of transactions between financial intermediaries now occurs in a way similar to ETD markets.

- Although useful, this systemic credit risk transfer from financial intermediaries to CCPs can lead to centralization and concentration of risks. Proper safeguards must be in place to avoid excessive risk being held in CCPs.

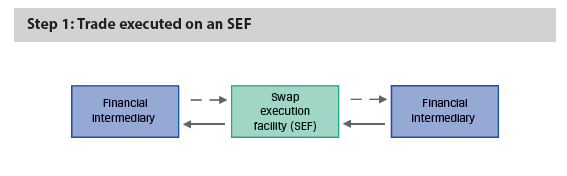

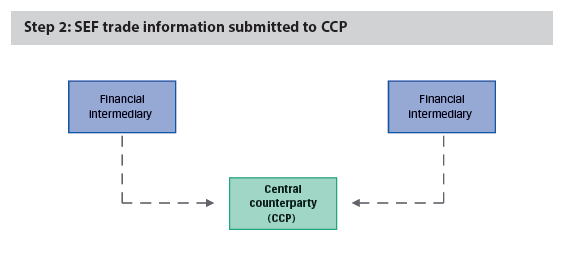

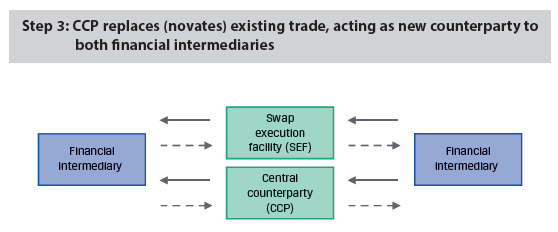

Exhibit 7 shows the 3-step central clearing process for interest rate swaps. The same process also applies to other derivative instruments.

In Step 1, a derivatives trade is executed on a swap execution facility (SEF), which is a swap trading platform that multiple dealers can access.

In Step 2, the original transaction details are shared with the CCP.

In Step 3, the CCP replaces the existing trade. The initial SEF contract is replaced by identical trades facing the CCP in this novation process. The CCP acts as a counterparty to both financial intermediaries, eliminating bilateral counterparty credit risk and providing clearing and settlement services.

Share on :

Do IFT Mocks to make you exam-ready!

Do IFT Mocks to make you exam-ready!