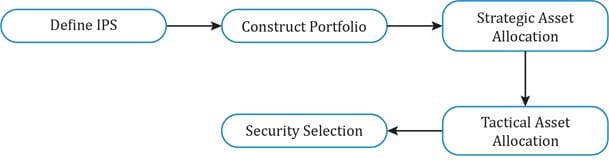

We have defined the IPS with return and risk objectives, and five constraints. Now, using the points in the IPS as a guideline, we need to construct the portfolio.

Portfolio construction consists of three steps:

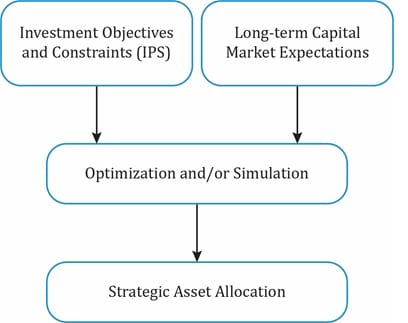

Capital market expectations are the investor’s expectations about the return and risk of various asset classes. Capital market expectations include the return for each asset class an investor may invest in (e.g., stock market, bond market, alternative investments, real estate, etc.), the standard deviation of returns for each asset class (risk), and the correlation between the asset classes.

The long-term capital market expectations and investor’s risk-return objectives are combined into a strategic asset allocation. This is accomplished through optimization and/or simulation on computer systems.

Strategic asset allocation is a strategy to allot a certain percentage of the portfolio, each to different IPS-permissible asset classes, in order to achieve the client’s long-term goals. Using this method, the portfolio manager decides how much of the client’s money should be invested in equities, bonds, or any other asset class to meet the client’s long-term goals. Strategic asset allocation is important because:

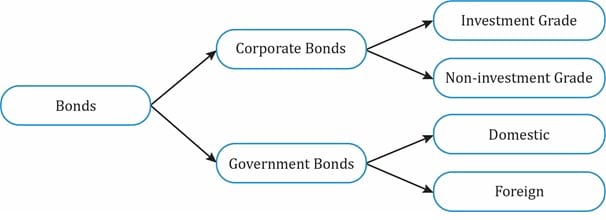

How are asset classes defined?

The classification of asset classes is somewhat subjective. Furthermore, an asset class can be divided into sub-asset classes as illustrated below.

Criteria to define asset classes:

When defining the SAA, it is important to consider the asset class correlation matrix. When the correlation between asset classes is low, the diversification benefit will be high. This concept has been discussed in detail in earlier readings.

Example

Given the matrix below, identify which asset class is most sharply distinguished from equities.

Historical correlation (May 31, 2005 to April 30, 2009)

| Equities | Fixed Income | Hedge | Real Estate | Private Equity | Commodities | Currencies | |

| Equities | 1.00 | ||||||

| Fixed Income | -0.35 | 1.00 | |||||

| Hedge | 0.64 | -0.35 | 1.00 | ||||

| Real Estate | 0.88 | -0.21 | 0.58 | 1.00 | |||

| Private Equity | 0.88 | -0.30 | 0.65 | 0.92 | 1.00 | ||

| Commodities | 0.38 | -0.37 | 0.60 | 0.29 | 0.45 | 1.00 | |

| Currencies | 0.18 | 0.16 | 0.19 | 0.16 | 0.16 | 0.26 | 1.00 |

Source: FT Alphaville

Solution:

The question asks us to identify the asset class with the lowest correlation with equities. As you can see from the table, fixed income has the lowest correlation with equities while real estate and private equity have the highest correlation with equities.

Once the asset allocation is done, it is possible for this asset allocation to drift from the target allocation with time. For example, let us assume the target asset allocation is 60 percent in stocks and 40 percent in bonds. If equities do well the following year, the asset allocation drifts to 90 percent in equities and 10 percent in bonds. This calls for rebalancing the portfolio as the drift is substantial. By rebalancing, we mean sell equities and buy bonds to bring the portfolio back to the target asset allocation. The amount of allowable drift and rebalancing policy should be defined in the IPS appendix. This material will be covered in detail at Level III.

Portfolio construction involves the following steps:

Some additional terms you should know:

Two new developments in portfolio management are:

ESG implementation approaches require a set of instructions for investment managers regarding selection of securities, the exercise of shareholder rights and the selection of investment strategies.

ESG implementation approaches affects both strategic asset allocation and the portfolio construction process. They may have a negative impact on expected risk and return of a portfolio as it may limit the manager’s investment universe and the manner in which investment management firms operate. Nonetheless, ESG investing continues to see strong adoptions. Responsible investing proponents argue that the potential improvements in governance and avoidance of material risks will enhance returns. Academic research on the impact of ESG factors on portfolio returns remains mixed.

Ace the Exam with IFT Notes!

Ace the Exam with Active Learning!

Do IFT Mocks to make you exam-ready!

Do IFT Mocks to make you exam-ready!

Practice your way to success!

Accelerate your studies!

Sign up to get more!