Historical return is the return actually earned in the past, while expected return is the return one expects to earn in the future.

Historical data shows that higher returns were earned in the past by assets with higher risk. Of the three major asset classes in the U.S., namely stocks, bonds, and T-bills, it has been observed that stocks had the highest risk and return followed by bonds, and T-bills had the lowest return and lowest risk.

|

Asset Class |

Annual Average Return | Standard Deviation (Risk) |

| Small-cap stocks |

High ↓Low |

High ↓Low |

| Large-cap stocks | ||

| Long-term corporate bonds | ||

| Long-term treasury bonds | ||

| Treasury bills |

In evaluating investments using mean and variance, we make the following two assumptions:

Risk aversion refers to the behavior of investors preferring less risk to more risk.

Risk tolerance is the amount of risk an investor is willing to take for an investment. High risk aversion is the same as low risk tolerance. Three types of risk profiles are outlined below:

The utility of an investment can be calculated as:

Utility = E(r) – 0.5 x A x ?2

where:

A = measure of risk aversion (the marginal benefit expected by the investor in return for taking additional risk. A is higher for risk-averse individuals.

𝜎2 = variance of the investment

E(r) = expected return

Instructor’s Note:

While using this formula, use only decimal values for all parameters.

Example

An investor with A = 2 owns a risk-free asset returning 5%. What is his utility?

Solution:

Utility = 0.05 – 0.5 x 2 x 0 = 0.05

Now, he is considering an asset with 𝜎 = 10%. At what level of return will he have the same utility?

0.05 = E(r) – 0.5 x 2 x 0.12. Solving for E(R) we get 0.06 or 6.00%.

Given a choice between a risk-free asset and stock with an expected return of 10% and 𝜎 = 20%, what will he prefer?

U = 0.1 – 0.5 * 2 * 0.22 = 0.06. Since the utility number of 0.06 is higher than 0.05, the investor will prefer this investment over the previous one.

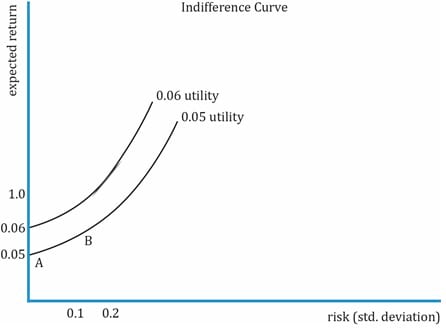

Indifference Curves

The indifference curve is a graphical representation of the utility of an investment. An indifference curve plots various combinations of risk-return pairs that an investor would accept to maintain a given level of utility. If the combinations of risk-return on a curve provide the same level of utility, then the investor would be indifferent to choosing one. Each point on an indifference curve shows that the investor is indifferent to what investment he chooses (risk/return combination) as long as the utility is the same.

To understand the indifference curve, let us plot all these numbers – expected return, standard deviation, and utility – on a graph.

The key points to note are:

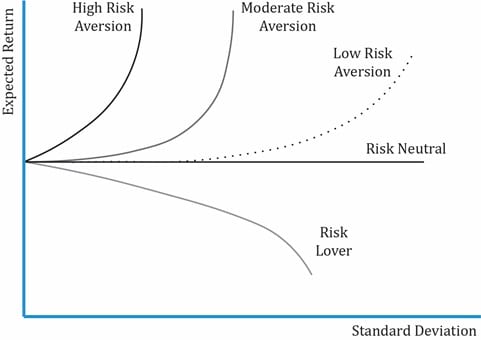

We now consider the indifference curves for different types of investors.

The exhibit above shows the indifference curves for different types of investors with expected return on y-axis and standard deviation on x-axis. Note the following:

Now that we have seen utility theory and indifference curves for various investors, let us see how to apply it in portfolio selection. The simplest case is when a portfolio comprises two assets: a risk-free asset and a risky asset. For a high-risk averse investor, the choice is easy, to invest 100% in the risk-free asset but at the cost of lower returns. Similarly, for a risk-lover it would be to invest 100% in the risky asset. But is it the optimal allocation of assets, or can there be a trade-off?

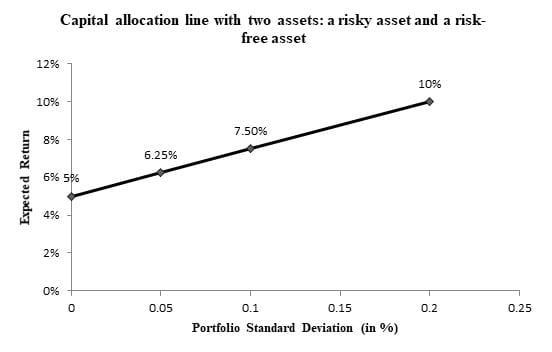

Example

Consider a simple portfolio of a risk-free asset and a risky asset. Plot the expected return of the portfolio against the risk of the portfolio for different weights of the two assets.

| Risk-free asset | Risky asset |

| Rf = 5% | Ri = 10% |

| ? = 0 | ?i = 20% |

Solution:

A portfolio’s standard deviation is calculated as:

Given that ?1 = 0, the terms become zero as the correlation between a risk-free asset with risky asset is zero.

become zero as the correlation between a risk-free asset with risky asset is zero.

So, the equation becomes ?p = w2 * ?2. For different weights of the risky asset, let’s calculate the values for risk and return and plot portfolio risk-return on a graph. Note that the expected return is a weighted average of the two assets.

| Weight of risky asset = w2 | ?p (portfolio risk) = w2 * ?2 | Rp (Portfolio return) = w1* Rf + w2 * Ri |

| 0 | 0 | 5% |

| 0.25 | 5% | 6.25% |

| 0.5 | 10% | 7.5% |

| 1 | 20% | 10% |

Graph interpretation:

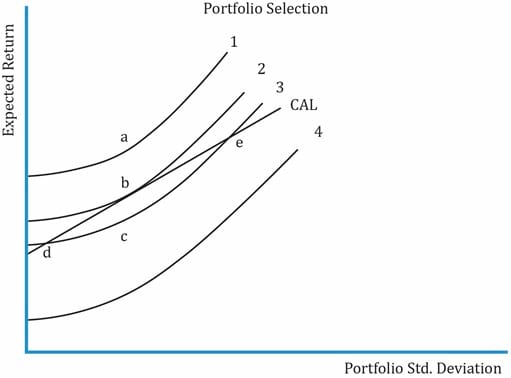

What is the Optimal Portfolio?

We get the optimal portfolio by combining the indifference curves and the capital allocation line. The utility theory gives us the indifference curves for an individual, while the capital allocation lines give us a set of feasible investments. The optimal portfolio for an investor will lie somewhere on the capital allocation line, i.e., some combination (weight) of the risky asset and risk-free asset. Using an investor’s risk-aversion measure A, we can use the utility theory to plot the indifference curves for an individual. Assume the indifference curves for this investor look as shown in the exhibit below:

Some key points about the graph:

If another investor has a higher level of risk aversion, where will his optimal portfolio lie? With a higher risk aversion level, the indifference curves will be steeper. The tangential point will be closer to the risk-free asset, so it will be to the south-west of point b.

Ace the Exam with IFT Notes!

Ace the Exam with Active Learning!

Practice your way to success!

Accelerate your studies!

Do IFT Mocks to make you exam-ready!

Do IFT Mocks to make you exam-ready!

Sign up to get more!