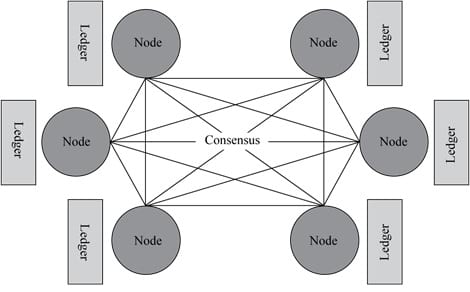

A distributed ledger is a database which can be shared across computer entities (or nodes) in a network. This is illustrated in Exhibit 5 from the curriculum.

There can be thousands of nodes in a network. Every node will have a copy of the distributed ledger. There is a consensus mechanism which ensures that all these ledgers are kept in sync. Through the consensus mechanism all nodes agree on a new transaction and update their ledgers. New records are considered immutable, which means once a record is created it cannot be changed.

DLT uses cryptography, which refers to encrypting and decrypting data. Through encryption, we ensure that the data remains secure.

DLT also accommodates smart contracts. These are computer programs that self-execute on the basis of pre-specified terms and conditions. For example, contracts that automatically transfer collateral from the borrower to the lender in the event of default.

DLT networks allow us to create, exchange, and track ownership of financial assets on a peer-to-peer basis. There is no central authority to validate the transactions.

DLT benefits include:

Blockchain is a type of distributed ledger. Its characteristics are:

The following steps outline the process of adding new transactions to the Blockchain network.

DLT can take the form of permissionless or permissioned networks.

Permissionless networks are open to any user who wishes to make a transaction. Once a transaction is added, it cannot be changed. All users can see all transactions on the block chain. These networks do not depend on a central authority.

In permissioned networks, network members may be restricted from participating in certain network activities. Controls or permissions might be used. Different users may have different levels of access to the ledger.

Cryptocurrencies:

They are also called digital currency or electronic currency. These do not have any physical form, but allow transactions to take place between buyers and sellers. They are issued by private individuals or organizations. There is no central authority, like a central bank backing these currencies.

Many cryptocurrencies have a self-imposed limit on the total amount of currency they may issue. For example, a well-known cryptocurency, Bitcoin has a self-imposed limit of 21 million.

We should also recognize the fact that with cryptocurrencies there is a lack of fundamentals underlying the value of the currency. Hence, they tend to be very volatile relative to major currencies like the Dollar or the Euro.

An initial coin offering (ICO) is an unregulated process whereby companies sell their crypto-tokens to investors. Through this process, investors fund the company and the tokens can be used to buy products and services from the company at a latter point in time.

Tokenization:

It is the process of representing ownership rights to physical assets on a blockchain or distributed ledger. Usually transactions involving physical assets, such as real estate, require substantial efforts in ownership verification and examination. DLT can streamline this process by creating a single digital record of ownership.

Post-Trade Clearing and Settlement:

In the financial securities market, the post-trade clearing and settlement process is quite cumbersome. DLT has the ability to streamline this process by providing near-real-time trade verification, reconciliation, and settlement. This can significantly reduce the complexity, time, and cost involved with processing transactions.

Compliance:

Over the last few years regulators have made reporting requirements stricter. They also demand greater transparency and access to data. Due to this, the cost and time associated with compliance activities has gone up substantially. In fact, in many companies the number of staff employed in compliance departments has gone up.

DLT can streamline the compliance process and bring down these costs. It can allow firms and regulators to get near-real-time access to transaction data, as well as other relevant compliance data. This will help firms and regulators to quickly uncover fraudulent activities. DLT can also reduce compliance costs associated with know-your-customer and anti-money-laundering regulations which require verification of the identities of clients and business partners.

There are several challenges to DLT that need to be addressed before it is successfully adopted by the investment industry. They include:

Ace the Exam with IFT Notes!

Ace the Exam with Active Learning!

Accelerate your studies!

Do IFT Mocks to make you exam-ready!

Do IFT Mocks to make you exam-ready!

Practice your way to success!

Sign up to get more!