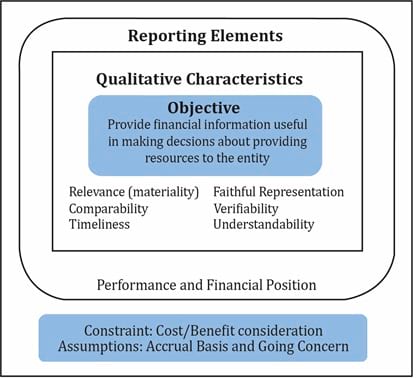

The IFRS has prepared a framework for the preparation and presentation of financial reports. The framework is shown in the diagram below.

Objective of financial statements

At the center of the framework is the objective of financial statements. As per the IFRS framework, the objective of financial statements is ‘to provide financial information about the reporting entity that is useful to existing and potential investors, lenders, and other creditors in making decisions about providing resources to the entity.’

The IASB Conceptual Framework for Financial Reporting is designed to:

Qualitative characteristics

Surrounding the objective are the desirable qualitative characteristics of financial statements.

The two fundamental qualitative characteristics are:

The four supplementary qualitative characteristics are:

Surrounding the qualitative characteristics are the reporting elements used to present information.

Elements related to measurement of financial position are:

Elements related to measurement of financial performance are:

Below the reporting elements are the constraints faced and the assumptions made while preparing financial statements.

Constraints

Assumptions

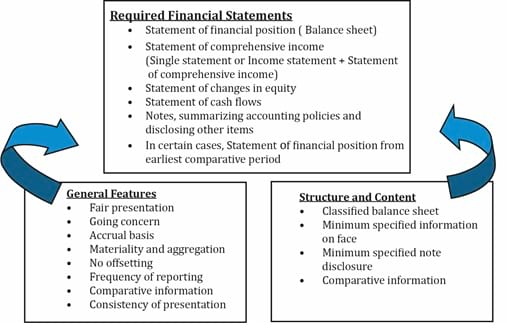

Required financial statements

The required financial statements are:

General features for preparing financial statements

The general features for preparing financial statements are:

Structure and content requirements

Firms should use the classified balance sheet structure (which shows current and non-current assets and liabilities separately.) Certain minimum information must be presented in the notes and on the face of the financial statements.

A significant percentage of listed companies use either IFRS or US GAAP. An analyst must be cautious when comparing financial measures between companies reporting under IFRS and companies reporting under US GAAP. If needed, specific adjustments need to be made to achieve comparability.

US GAAP uses standards issued by FASB while IFRS uses standards issued by IASB. While the two organizations are working towards convergence, significant differences still remain.

Differences between IFRS and US GAAP:

| Basis for Comparison | US GAAP | IFRS |

| Developed by | Financial Accounting Standard Board (FASB). | International Accounting Standard Board (IASB). |

| Based on | Rules | Principles |

| Inventory valuation | FIFO, LIFO and Weighted Average Method. | FIFO and Weighted Average Method. |

| Extraordinary items | Shown below (at the bottom of the income statement). | Not segregated in the income statement. |

| Development cost | Treated as an expense | Capitalized, only if certain conditions are satisfied. |

| Reversal of Inventory | Prohibited | Permissible, if specified conditions are met. |

Source: CFAI Curriculum 2020; https://keydifferences.com/difference-between-gaap-and-ifrs.html

Analysts must be aware that reporting standards are evolving rapidly. They need to monitor developments in financial reporting and assess their implications for security analysis and valuation.

A financial analyst can remain aware of developments in financial reporting standards by monitoring three sources:

Ace the Exam with IFT Notes!

Ace the Exam with Active Learning!

Practice your way to success!

Do IFT Mocks to make you exam-ready!

Do IFT Mocks to make you exam-ready!

Accelerate your studies!

Sign up to get more!