This reading brings us to the end of financial reporting and analysis. Think of this reading as a practical application of steps outlined for a financial analysis framework (define purpose, collect and process data, analyze and interpret, recommend and follow-up). Some of the questions we will address over the next few sections are:

Evaluating past performance helps analysts assess how the company performed and the reasons behind its performance (why it performed the way it did). When studying a company, some key analytical questions include the following:

To evaluate how a company performed, an analyst can process data by creating common-size financial statements, calculating ratios, and analyzing industry-specific metrics. Some of the factors an analyst must be aware of when evaluating financial performance are discussed below:

Change in Company’s Strategy

The effect of a company’s strategy is reflected in its performance. Let us take the example of Apple Inc.

Differences in Accounting Standards

When comparing the ratios of different companies, analysts must be aware of the accounting standards, methods, and estimates used for reporting as they can have a significant impact on the financial statements. Let us consider the example below where the ROE of three companies reporting under different accounting standards are given. For comparison, they are then converted to US GAAP.

| ROE of three companies for a year (in %) | |||

| Mexican GAAP | Brazilian GAAP | US GAAP | |

| Mexican company | 52.69 | 211.12 | |

| Brazilian company | -7.89 | 29.34 | |

| U.S. company | 12.69 | ||

While the Mexican company reported the highest ROE under Mexican and US GAAP, the Brazilian company turned profitable under US GAAP after posting a negative ROE. The table illustrates why it is important to make adjustments to a common standard such as US GAAP before comparing the financial ratios of companies.

This comparison only provides information about how a company performed. To understand why it performed better or worse, analysts gather information from the management commentary, MD&A, and industry sources such as consumer surveys. The results of a past performance analysis set the ground for making recommendations.

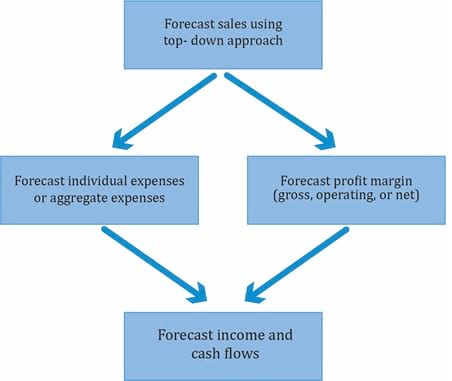

To estimate the target price for a company’s stock, an analyst needs to forecast EPS. The inputs for estimating EPS are future sales and profit. The steps usually followed for projecting performance are illustrated below:

Notice that future income can be projected in two ways: by estimating expenses and by forecasting future profit margins. The individual steps used to forecast sales and profit margin are listed below:

Forecast Sales

Analysts often take a top-down approach to forecasting sales.

Forecast Expenses

Forecast Cash Flows

Instructor’s Note: Section 3 ‘Projecting Multiple-Period Performance’ is not testable and hence not covered.

Another application of financial statement analysis is in assessing the credit risk of a borrower. Credit risk is the risk that the borrower will fail to make the obligated interest and principal payments. Credit analysis is the evaluation of credit risk. The purpose of credit analysis is to determine whether a company will be able to service its debt (interest and principal payments) on time. A credit analysis exercise is likely to include an evaluation of the following:

Let us take a look at how Moody’s assigns credit ratings for a company based on the following groups of qualitative factors:

Ace the Exam with Active Learning!

Ace the Exam with IFT Notes!

Practice your way to success!

Do IFT Mocks to make you exam-ready!

Do IFT Mocks to make you exam-ready!

Accelerate your studies!

Sign up to get more!