There are two main interrelated concepts that will be discussed in detail in this reading: financial reporting quality and earnings quality.

Financial reporting quality: High-quality financial reporting provides information that is useful to analysts in assessing a company’s performance and prospects. They contain information that is relevant, complete, neutral, and free from error.

High-quality reporting helps in making the right decision as it depicts the true economic reality of a company for the reporting period. Low-quality financial reporting contains inaccurate, misleading, or incomplete information.

Earnings quality: High-quality earnings result from activities that a company will likely be able to sustain in the future and provide a sufficient return on the company’s investment. If the return on investment is greater than the cost of funds, then it indicates high earnings quality.

Sustainability is the key here. For example, assume a company uses accrual-based earnings in a quarter. It has high accounts receivable and as a result reports high earnings, which is not sustainable in the following quarters. This implies earnings quality is low.

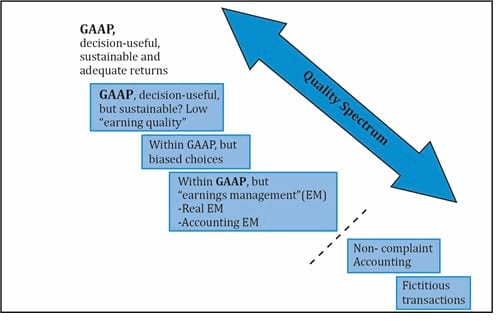

Combining the two aspects – financial reporting quality and earnings quality, we get a spectrum spanning from highest to lowest. Let us now look at the characteristics of reporting/earnings quality as we move down along the spectrum as shown in the exhibit below.

Non-GAAP reporting of financial metrics which is not in compliance with generally accepted accounting principles such as US GAAP and IFRS includes both financial metrics and operating metrics. Non-GAAP earnings are sometimes referred to as underlying earnings, adjusted earnings, recurring earnings, or core earnings.

The choice of accounting methods used can distort the economic reality. Unbiased financial reporting is the ideal, but investors may prefer conservative accounting choices as a positive surprise is acceptable. Whereas the management may prefer aggressive accounting choices.

Aggressive accounting: It refers to biased accounting choices that aim to improve the reported earnings or financial position in the period under review.

Conservative accounting: It refers to biased accounting choices that aim to decrease the reported earnings or financial position in the reporting period.

Some managers use aggressive accounting when earnings are below targets and conservative accounting when earnings are above targets, to artificially smooth earnings.

When a company makes conservative choices, it implies that:

Ace the Exam with Active Learning!

Ace the Exam with IFT Notes!

Accelerate your studies!

Do IFT Mocks to make you exam-ready!

Do IFT Mocks to make you exam-ready!

Practice your way to success!

Sign up to get more!