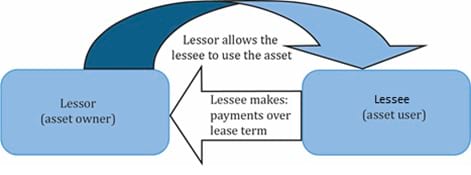

A lease is a contract in which a lessor grants the lessee the exclusive right to use a specific underlying asset for a period of time in exchange for payments.

Below is a pictorial representation of what constitutes a lease. An asset’s owner is called a lessor. The entity or person wishing to use the asset is called the lessee. The lessor allows the lessee to use the asset for a pre-determined period. In return, the lessee makes periodic payments to the lessor over the period for the right to use the asset. This period can be as long as 20 years, or as short as a month.

Not testable

Following are some of the advantages to leasing an asset compared to purchasing it.

Leases are classified as finance or operating. A finance lease is similar to purchasing an asset while an operating lease is similar to renting an asset.

A lease is classified as a finance lease if any of the following five criteria are met.

If none of the criteria are met, then the lease is classified as an operating lease.

The financial reporting of leases depends on:

US GAAP and IFRS share the same accounting treatment for lessors but differ for lessees.

IFRS has a single accounting model for both operating leases and finance lease lessees, while US GAAP has different accounting models for each.

Under IFRS, there is a single accounting model for both finance and operating leases for lessees.

(Although the lease liability and ROU begin with the same carrying value, their balance sheet values tend to diverge over time because of the differences in the calculation of principal repayments that reduces the lease liability and the amortization expense that reduces the ROU asset.)

The following list shows how the lease transaction affects the financial statements.

Example: Lessee Accounting – IFRS

(This is based on Example 11 from the curriculum.)

A company is offered the following terms to lease a machine: five-year lease with an implied interest rate of 10% and an annual lease payment of EUR100,000 per year payable at the end of each year. PV = EUR379,079. The asset will be amortized over the five-year lease term on a straight-line basis. The company reports under IFRS.

What would be the impact of this lease on the company’s:

Solution to 1:

The company will report a lease liability and a ROU asset of EUR379,079.

Solution to 2:

In Year 2, the company will report an interest expense of EUR31,699 and an amortization expense of EUR 75,816.

The calculations are shown in the tables below:

| Lease Payment | Interest Expense (10% × Lease Liability) |

Principal Repayment (Payment – Interest) |

Lease Liability | |

| FO.1 | FO.2 | FO.3 | FO.4 | |

| Year 0 | 379,079 | |||

| Year 1 | 100,000 | 37,908 | 62,092 | 316,987 |

| Year 2 | 100,000 | 31,699 | 68,301 | 248,685 |

| Year 3 | 100,000 | 24,869 | 75,131 | 173,554 |

| Year 4 | 100,000 | 17,355 | 82,645 | 90,909 |

| Year 5 | 100,000 | 9,091 | 90,909 | 0 |

| Total | 500,000 | 120,921 | 379,079 |

| Amortization Expense | ROU Asset | |||||||

| Straight-Line F.1 | F.2 | |||||||

| Year 0 | 379,079 | |||||||

| Year 1 | 75,816 | 303,263 | ||||||

| Year 2 | 75,816 | 227,447 | ||||||

| Year 3 | 75,816 | 151,631 | ||||||

| Year 4 | 75,816 | 75,816 | ||||||

| Year 5 | 75,816 | 0 | ||||||

| Total | 379,079 | |||||||

Solution to 3:

In Year 2, principal repayment of EUR68,301 will be reported as a cash outflow under financing activities. The interest expense of EUR31,699 may be reported under operating or financing activities depending on the company’s reporting policies.

Under US GAAP, there are two accounting models for lessees: one for finance leases and another for operating leases.

The finance lease accounting model is the same as the lease accounting model for IFRS.

The operating lease accounting model is different:

(Since the principal repayment and amortization are calculated in the same way, the lease liability and the ROU asset will always equal each other)

The following list shows how the lease transaction affects the financial statements.

For a US GAAP company classifying a lease as an operating lease instead of a finance lease affects the financial ratios as shown below:

| Ratio | Formula | Impact of Using an Operating Lease Instead of a Finance Lease |

| EBITDA margin | Lower: Lease expense is classified as an operating expense rather than interest and amortization. | |

| Asset turnover | Lower: Total assets are higher under an operating lease because the ROU asset is amortized at a slower pace in initial years. | |

| Cash flow per share | Lower: Cash flow from operations is lower because the entire lease payment is included in operating activities versus solely interest expense for a finance lease. |

The accounting for lessors is identical under IFRS and US GAAP. However, the accounting differs based on whether the lease is a finance lease or an operating lease.

Finance lease lessors (IFRS and US GAAP)

The following list shows how the lease transaction affects the financial statements.

Operating lease lessors (IFRS and US GAAP)

The following list shows how the lease transaction affects the financial statements.

Example: Lessor Accounting

(This is based on Example 13 from the curriculum.)

Let’s examine the previous example from the perspective of the lessor. Assume that the carrying value of the asset immediately prior to the lease is EUR350,000, accumulated depreciation is zero, and the lessor elects to depreciate it on a straight-line basis over five years.

How would the lessor’s financial statements be affected by the classification of the lease as a finance or operating lease?

Solution:

Balance sheet: The difference on the balance sheet is material. The present value of lease payments is well above the carrying value of the asset. The finance lease classification therefore results in a significant increase in assets.

| Balance Sheet | Year 1 | Year 2 | Year 3 | Year 4 | Year 5 | ||||

| Finance lease: | |||||||||

| Lease receivable, net | 316,987 | 248,685 | 173,554 | 90,909 | 0 | ||||

| Operating lease: | |||||||||

| Property, plant, and equipment, net | 280,000 | 210,000 | 140,000 | 70,000 | 0 | ||||

Income statement: The difference on the income statement is also material.

| Income Statement | Year 1 | Year 2 | Year 3 | Year 4 | Year 5 |

| Finance lease: | |||||

| Interest

revenue |

37,908 | 31,699 | 24,869 | 17,355 | 9,091 |

| Operating lease

: |

|||||

| Lease revenue | 100,000 | 100,000 | 100,000 | 100,000 | 100,000 |

Cash flow statement: The cash flow statement is the same under both options.

| Statement of Cash Flows | Year 1 | Year 2 | Year 3 | Year 4 | Year 5 | |

| Finance lease: | ||||||

| Cash flows from operating activities | 100,000 | 100,000 | 100,000 | 100,000 | 100,000 | |

| Operating lease: | ||||||

| Cash flows from operating activities | 100,000 | 100,000 | 100,000 | 100,000 | 100,000 | |

Ace the Exam with Active Learning!

Ace the Exam with IFT Notes!

Do IFT Mocks to make you exam-ready!

Do IFT Mocks to make you exam-ready!

Accelerate your studies!

Practice your way to success!

Sign up to get more!