Equity is the owners’ residual claim on a company’s assets after subtracting its liabilities.

The six components of equity are:

The statement of changes in equity presents information about the increases or decreases in a company’s equity over a period of time. IFRS requires the following information in the statement of changes in equity:

U.S. GAAP requirement is for companies to provide an analysis of changes in each component of equity as shown in the balance sheet.

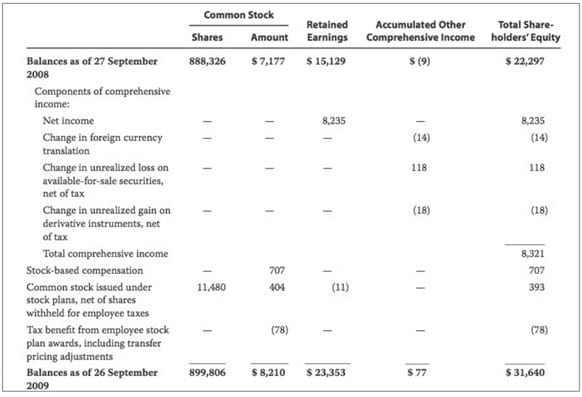

Sample Statement of Changes in Stockholders’ Equity

Share on :

Do IFT Mocks to make you exam-ready!

Do IFT Mocks to make you exam-ready!