Managers may be motivated to issue financial reports that are not high quality in order to:

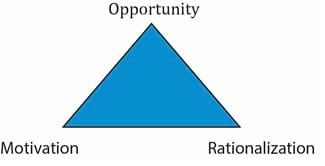

The three conditions conducive for issuing low-quality financial reports are presented below:

Opportunity: It can be the result of weak internal controls, ineffective board of directors, and accounting standards that allow a range of choices.

Motivation: It can result from pressure to meet some criteria for some personal reasons.

Rationalization: It can result from justifying a wrong choice as seen in Enron’s case. Enron’s CFO sought board approvals, legal and accounting opinions for misstated financial statements.

Market Regulatory Authorities

Regulators in every country can play a key role in enforcing financial reporting quality. Examples of regulatory authorities include:

These regulatory authorities are members of an international organization called the International Organization of Securities Commissions (IOSCO), comprising 120 regulatory authorities and 80 securities market participants like the stock exchanges.

The actual regulation, however, is enforced through each individual regulatory authority in a country. The features of any regulatory regime such as the SEC that affect financial reporting quality include the following:

Auditors

Financial statements of public companies must be audited by an independent auditor. Auditors issue opinions on the financial statements of the company and on the effectiveness of the companies’ internal controls. An unqualified opinion on the financial statements indicates that the financial statements present fairly the company’s performance in accordance with relevant standards. Key audit matters discuss matters of most significance in the audit of the financial statements of the current period.

However, there are some drawbacks of audited opinion:

Private Contracting

We have seen earlier that managers are motivated to manipulate earnings in order to avoid violating debt covenants or triggers that may prompt investors to recover all or part of their investment.

Consider an example where a company takes a loan from a bank; there is every incentive for the company to dress up its financial reports to keep its cost of capital low. So it is in the best interest of investors, such as the bank here, to monitor the quality of financial reports and detect any misreporting.

Ace the Exam with IFT Notes!

Ace the Exam with Active Learning!

Accelerate your studies!

Practice your way to success!

Do IFT Mocks to make you exam-ready!

Do IFT Mocks to make you exam-ready!

Sign up to get more!