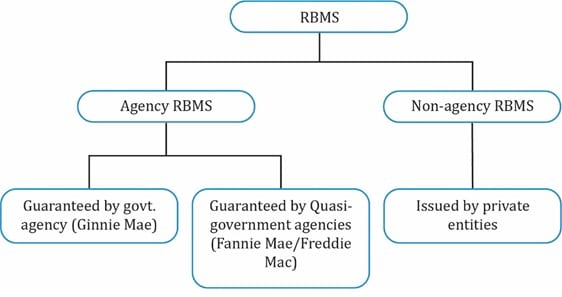

Residential mortgage-backed securities are bonds created from the securitization of residential mortgage loans. In the U.S., residential mortgage-backed securities are divided into the following three sectors:

The first two sectors (guaranteed by the government or a quasi-government entity) are called the agency RMBS. The third sector is called non-agency RMBS.

Examples of agency RMBS include:

The two differences between agency RMBS issued by GSEs and non-agency RMBS are as follows:

A mortgage pass-through security is created when one or more holders of mortgages form a pool of mortgages and sell shares or participation certificates in the pool. The investors receive a share of cash flows from the underlying pool of mortgage loans.

Cash Flow Characteristics

How is the rate and maturity of a mortgage loan calculated?

Conforming and Non-conforming Loans

A mortgage loan must meet certain criteria to be included in a pool of loans backing an RMBS. Listed below are some of the underwriting standards of an agency they must conform to:

If a loan meets the underwriting standards, then it is called a conforming loan.

Non-conforming mortgages that serve as collateral for mortgage pass-through securities do not meet the underwriting standards and are privately issued by thrift institutions, commercial banks, etc.

Example

Assume that a pool includes four mortgages with the following characteristics:

| Mortgage | Outstanding Balance | Coupon Rate | Time to Maturity |

| 1 | $1,000 | 4.50% | 28 months |

| 2 | $2,000 | 4.75% | 42 months |

| 3 | $4,000 | 5.15% | 37 months |

| 4 | $3,000 | 3.80% | 60 months |

Calculate the weighted average coupon rate and weighted average maturity.

Solution:

The total outstanding amount is $10,000 and hence, the weights are as follows: Mortgage 1 = 10%, 2 = 20%, 3 = 40% and 4 = 30%.

The weighted average coupon is:

The weighted average maturity (WAM) is:

Prepayment risk: The risk associated with uncertainty in future cash flows because of principal repayments is called prepayment risk. It has two components: contraction risk and extension risk.

Instructor’s Note

Contraction risk occurs when interest rates decline.

Extension risk occurs when interest rates rise.

Prepayment Rate Measures

To value a mortgage pass-through security, one must be able to forecast its cash flows. But, the cash flows are uncertain because it is not known ahead of time when homeowners may prepay principal during the mortgage’s life. The only way to predict future cash flows is by making some assumptions about the prepayment speed/rate.

The two measures of prepayment rate are:

Single month mortality (SMM) measures prepayments in a month. An SMM of x% means that x% of the outstanding mortgage balance at the start of the month minus the scheduled principal repayment, will be repaid that month.

Conditional repayment rate (CPR) is an annualized version of SMM.

A CPR of 6%, for example, means that approximately 6% of the outstanding mortgage balance at the beginning of the year is expected to be prepaid by the end of the year.

100 PSA prepayment benchmark: The 100 Public Securities Association (PSA) prepayment benchmark is expressed as a monthly series of CPRs. The benchmark assumes that prepayment rates are low for newer mortgages and increase as time passes. A PSA assumption greater than 100 PSA means that prepayments are assumed to be faster than the benchmark. In contrast, a PSA assumption lower than 100 PSA means that prepayments are assumed to be slower than the benchmark.

Cash Flows

The cash flows associated with a mortgage pass-through security have the following components:

The interest payment is based on the principal outstanding at the start of the period and the interest rate. The principal pre-payment can be estimated based on the SMM (or CPR) number. The higher the SMM, the higher the prepayment.

Instructor’s Note

The curriculum shows the cash flow calculations for a hypothetical mortgage pass-through security. If you have the time you can study the curriculum example. However, from a testability perspective it is more important that you understand the concept which is explained here.

Weighted Average Life

Recall that one of the basic characteristics of a bond is its maturity. But, in the case of a MBS the legal maturity date does not reveal much about the characteristics of the security because of prepayments.

The weighted average life (average life) gives investors an indicator of how long investors can expect to hold the MBS before it is paid off. The table below shows the average life at different prepayment rates. For instance, at a prepayment rate of 125 PSA, the average time for principal repayment is 10.1 years. Notice that the average time drops drastically to 3.2 years as the prepayment rates go up to 600 PSA.

| PSA assumption | 100 | 125 | 165 | 250 | 400 | 600 |

| Average life (years) | 11.2 | 10.1 | 8.6 | 6.4 | 4.5 | 3.2 |

Ace the Exam with Active Learning!

Ace the Exam with IFT Notes!

Do IFT Mocks to make you exam-ready!

Do IFT Mocks to make you exam-ready!

Accelerate your studies!

Practice your way to success!

Sign up to get more!