A wide range of assets apart from mortgage loans are used as collateral for asset-backed securities. The most popular non-mortgage ABS are auto loan receivable-backed securities and credit card receivable-backed securities. Based on the way the collateral pays, ABS can be categorized into two types: amortizing and non-amortizing.

Examples of amortizing loans backing an ABS: mortgage loans and automobile loans.

An example of non-amortizing loans backing an ABS: credit card receivables.

ABS must offer credit enhancement to be appealing to investors.

Cash flows consist of interest payment, scheduled principal repayments and any prepayments. For securities backed by auto loan receivables, prepayments result from any of the following:

All auto-loan backed securities have some form of credit enhancement such as:

Credit cards such as Visa and MasterCard are used to finance the purchase of goods and services, as well as for cash advances. When a cardholder makes a purchase using a credit card, he is agreeing to repay the amount borrowed (purchase amount) to the issuer of the card within a certain period, typically a month. If the outstanding amount is not repaid within this grace period, then a finance charge (interest rate) is applied to the balance not paid in full each month.

Credit card receivables are pooled together to act as a collateral for credit card receivable-backed securities. Cash flow, on a pool of credit card receivables consists of:

Characteristics of Credit Card Receivable-backed Securities

Payment Structure

Amortization Provision

There are two differences between credit card receivable-backed securities and auto loan receivable-backed securities:

A collateralized debt obligation is a generic term used to describe a security backed by a diversified pool of one or more debt obligations (e.g., corporate and emerging market bonds, leveraged bank loans, ABS, RMBS, CMBS, or CDO).

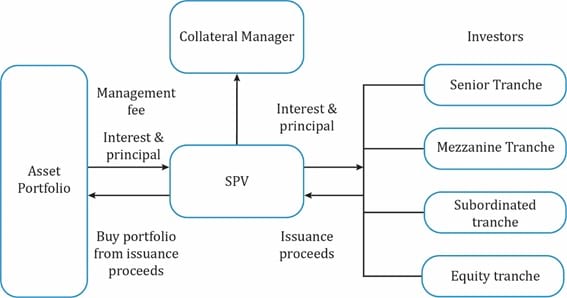

Like an ABS, a CDO involves the creation of a SPV. But, in contrast to an ABS, where the funds necessary to pay the bond classes come from a pool of loans that must be serviced, a CDO requires a collateral manager to buy and sell debt obligations, for and from the CDO’s portfolio of assets, to generate sufficient cash flows to meet the obligations of the CDO bondholders, and to generate a fair return for the equity holders.

The structure of a CDO includes senior, mezzanine, and subordinated/equity bond classes. The whole process is illustrated below:

The key components of a CDO structure are as follows:

Consider the following $100 million CDO. The collateral consists of bonds with a par value of $100 million paying a fixed rate of 11%.

| Tranche | Par value (US $) | Coupon rate |

| Senior | 80,000,000 | Libor + 70 bps |

| Mezzanine | 10,000,000 | 9% |

| Subordinated/equity | 10,000,000 | – |

Since the senior tranche requires a floating rate payment, the CDO manager enters into an interest rate swap with another party for a notional amount of $80 million paying a fixed rate of 8% and receiving Libor. This removes any uncertainty with respect to interest rate movements.

Let us now evaluate the cash flows for each party.

| Party | Type of cash flow | Amount |

| Collateral | Pays interest each year. Coupon rate = 11% | .11 x 100,000,000 = 11,000,000 |

| Senior tranche | Interest paid to senior tranche: Libor + 70 bps | (Libor + 70bps) x 80,000,000 = Libor x 80,000,000 + 560,000 |

| Mezzanine tranche | Interest paid: 9% | 0.09 x 10,000,000 = 900,000 |

| Interest rate swap | CDO to swap counterparty: 8% | 0.08 x 80,000,000 = 6,400,000 |

| Interest rate swap | From swap counterparty to CDO: Libor | 80,000,000 x Libor |

| Total interest received | 11,000,000

+ Libor x 80,000,000 |

|

| Total interest paid | Libor x 80,000,000 + 560,000

+ 900,000 + 6,400,000 = 7,860,000 + Libor x 80,000,000 |

|

| Net interest = Interest received – interest paid | 3,140,000 |

From the net interest available, the CDO manager’s fees must be paid. If the fees are 640,000, then the cash flow available to the subordinated/equity tranches is 3,140,000 – 640,000 = 2,500,000. The annual return for this tranche with a par value of $10 million is 2,500,000/10,000,000 = 25%

CDOs: Risks and Motivations

In the case of defaults in the collateral, there is a risk that the manager will fail to earn a return sufficient to pay off the investors in the senior and mezzanine tranches. Investors in the subordinated/equity tranche risk the loss of their entire investment.

Covered bonds are senior debt obligations issued by a financial institution and backed by a segregated pool of assets that typically consist of commercial or residential mortgages or public sector assets.

Covered bonds are similar to ABS, but they differ because of their:

Because of these additional safety features, covered bonds usually have lower credit risks and therefore lower yields as compared to otherwise similar ABS.

Ace the Exam with Active Learning!

Ace the Exam with IFT Notes!

Practice your way to success!

Do IFT Mocks to make you exam-ready!

Do IFT Mocks to make you exam-ready!

Accelerate your studies!

Sign up to get more!