Primary bond markets are markets in which bonds are sold for the first time by issuers to investors to raise capital. Bonds can be sold initially via a public offering or a private placement. Secondary bond markets are markets in which existing bonds are subsequently traded among investors. After the initial offering, bonds are bought and sold among investors in the secondary market.

A company/government/any entity issues bonds in two ways: public offering and private placement.

Public Offerings

As the name indicates, in a public offering, any member of the public may invest in a new bond issue. The issuer does not sell bonds directly to each investor. Instead, the issuer avails the services of an intermediary called the underwriter to facilitate the selling (placement) process. The underwriter is usually an investment bank because banks have a good understanding of how to market a new issue, tap their networks to locate investors, and successfully place the issue.

The different bond issuing mechanisms are:

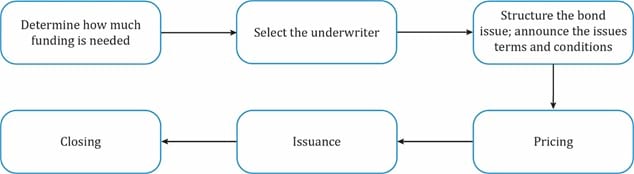

Underwritten offerings: In an underwritten offering, an investment bank negotiates an offering price with the issuer; the offering price is the price at which the issue will be sold. It then buys the entire issue at the offering price and takes the risk of reselling it to investors or dealers. Underwritten offering is also known as a firm commitment offering. The underwriting process is graphically depicted below:

Best effort offering: Contrary to an underwritten offering, in a best effort offering issue, the investment bank acts as a broker and only sells as many securities as it can instead of committing to sell 100% of the issue. The unsold bonds are returned to the issuer. The investment bank gets a commission for bonds sold at the offering price, faces less risk and has less incentive to sell the issue than in an underwritten offering. Best effort offering is usually preferred for riskier issues and corporate bonds.

Shelf registration: Shelf registration is a type of public offering where the issuer is not required to sell the entire issue at once. The issuer files a single document with regulators that describe a range of future issuances. The advantage is that the issuer does not have to prepare a new document for every bond issue provided there is no change in the issuer’s business and financial terms stated in the prospectus. This allows the issuer to save on repeated administrative expenses and registration fees.

Auctions: Government bonds across the world are usually sold to investors via an auction. Governments finance public debt by borrowing money through the central bank. An auction is a public offering method that involves bidding, and is helpful in price discovery and allocating securities. The United States follows a single-price auction method for its sovereign securities such as T-bills, T-notes, TIPS, etc. In this method, all winning bids pay the same price for the security and receive the same coupon rate.

Private Placement

As the name implies, the securities are not sold to the public in this type of funding. Instead, they are sold only to a select group of investors such as institutional investors. Other characteristics are as follows:

Securities are traded among investors in the secondary market. Large institutional investors and banks are the primary participants. Retail investors are limited here, unlike in the equities market.

Secondary bond markets are structured as organized exchanges or as over-the-counter markets.

It is important to understand the liquidity of a bond market:

Settlement is the process that occurs after a trade is made:

Sovereign bonds are issued by national governments primarily for fiscal reasons. Taxes are the primary source of revenue for a government. If tax revenue is insufficient, then a government raises money by issuing sovereign bonds.

Sovereign securities are classified into two categories based on when they were issued: on-the-run and off-the-run. On-the-run are recently issued sovereign securities that trade frequently. They are also called benchmark bonds because the yields of other bonds are determined relative to these bonds. Off-the-run refers to securities that were issued some time ago. They are less liquid compared to on-the-run securities.

Sovereign bonds are not backed by collateral. Instead, they depend on the taxing authority, i.e., the national government, to repay the debt. Rating agencies distinguish between a sovereign bond issued in local currency and one in foreign currency. Local currency bonds generally have a higher credit rating than foreign currency bonds, because if needed the national government can print local currency to repay the bond, however it cannot print the foreign currency.

Sovereign bonds can be fixed-rate, floating-rate or inflation-linked.

Ace the Exam with IFT Notes!

Ace the Exam with Active Learning!

Do IFT Mocks to make you exam-ready!

Do IFT Mocks to make you exam-ready!

Accelerate your studies!

Practice your way to success!

Sign up to get more!