The input variables for determining Macaulay and modified yield duration of fixed-rate bonds are:

By changing one of the above variables while holding others constant, we can analyze the properties of bond duration, which in turn, helps us assess the interest rate risk. We will use the formula for Macaulay duration to understand the relationship between each variable and duration:

![MacDur = [{\frac{1+r}{r} - \frac{1+r+[N*(c-r)]}{c*[(1+r)^N - 1]+r}] - \frac{t}{T}}](https://ift.world/wp-content/ql-cache/quicklatex.com-8e07eea33875d8c5e03155bb89f0edc1_l3.png "Rendered by QuickLaTeX.com")

The fraction of the coupon period that has gone by (t/T)

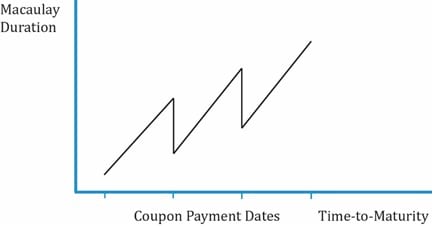

First, let us consider the relationship between fraction of time that has gone by (t/T) and duration. There is no change to the expression in braces {} as time passes by. Fraction of time (t/T) increases as time passes by. Assume T is 180. If 50 days have passed, then t/T = 0.277. If 90 days have passed, then t/T = 0.5. If 150 days have passed, then t/T = 0.83. As t/T increases from t = 0 to t = T with passing time, MacDuration decreases in value. Once the coupon is paid, t/T becomes zero and MacDuration jumps in value. When time to maturity is plotted against MacDuration, it creates a saw tooth pattern as shown graphically below:

Source: CFA Program Curriculum, Understanding Fixed-Income Risk and Return

Interpretation of the Macaulay duration between coupon payments with a constant yield to maturity:

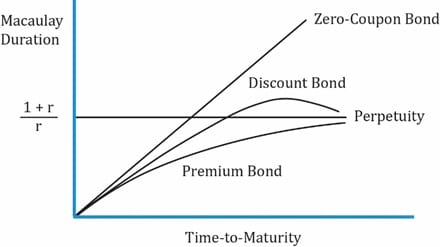

Now, we look at the relationship between Macaulay duration and change in the coupon rate, yield to maturity, and the time to maturity. This is depicted in the exhibit below:

Properties of the Macaulay Yield Duration

Time-to-Maturity

The relationship between Macaulay Duration and time-to-maturity for four types of bonds (zero-coupon, discount, premium, and perpetuity) at t/T = 0 are shown.

is a very large number. So

is a very large number. So  must be zero and the value in the numerator will not matter here. Macaulay duration of a perpetual bond is

must be zero and the value in the numerator will not matter here. Macaulay duration of a perpetual bond is  as N approaches infinity. because the second expression in braces is positive. As time passes, it approaches ., reaches a maximum and approaches (the threshold) from above. This happens when N is large and coupon rate (c) is below the yield-to-maturity (r). As a result, for a long-term discount bond, interest rate risk can be lesser than a shorter-term bond.

as N approaches infinity. because the second expression in braces is positive. As time passes, it approaches ., reaches a maximum and approaches (the threshold) from above. This happens when N is large and coupon rate (c) is below the yield-to-maturity (r). As a result, for a long-term discount bond, interest rate risk can be lesser than a shorter-term bond.The above points are summarized below:

| Relationship between bond duration and other input parameters | |

| Bond parameter | Effect on Duration |

| Higher coupon rate | Lower |

| Higher yield-to-maturity | Lower |

| Longer time-to-maturity | Higher for a premium bond. Usually, holds true for a discount bond, but there can be exceptions. Exception: low coupon (relative to YTM) bond with long maturity. |

Example 11: Calculating the approximate modified duration

A mutual fund specializes in investments in sovereign debt. The mutual fund plans to take a position on one of these available bonds.

| Bond | Time-to-Maturity | Coupon Rate | Price | Yield-to-Maturity |

| (A) | 5 years | 10% | 70.093879 | 20% |

| (B) | 10 years | 10% | 58.075279 | 20% |

| (C) | 15 years | 10% | 53.245274 | 20% |

The coupon payments are annual. The yields-to-maturity are effective annual rates. The prices are per 100 of par value.

Solution to 1:

Calculate PV+ and PV–; then calculate modified duration.

Bond A:

PV0 = 70.093879;

PV+ = 69.977386

70.210641

70.210641 = 70.210641

= 70.210641

= 3.33.

= 3.33.The approximate modified duration of Bond A is 3.33.

Bond B:

PV0 = 58.075279

= 57.937075

= 57.937075PV+ = 57.937075

= 58.213993

= 58.213993PV–= 58.213993

= 4.77

= 4.77The approximate modified duration of Bond B is 4.77.

Bond C:

PV0 = 53.245274

= 53.108412

= 53.108412PV+ = 53.108412

= 53.382753

= 53.382753PV– = 53.382753

= 5.15.

= 5.15.The approximate modified duration of Bond C is 5.15.

Solution to 2:

Bond C with 15 years-to-maturity has the highest modified duration. If the yield to maturity on each is decreased by the same amount – for instance, by 10bps, from 20% to 19.90% – Bond C would be expected to have the highest percentage price increase because it has the highest modified duration.

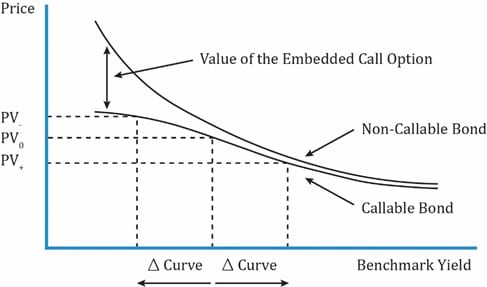

Interest Rate Risk Characteristics of a Callable Bond

A callable bond is one that might be called by the issuer before maturity. This makes the cash flows uncertain, so the YTM cannot be determined with certainty. The exhibit below plots the price-yield curve for a non-callable/straight bond and a callable bond. It also plots the change in price for a change in the benchmark yield curve. Bond price is plotted on the y-axis and the benchmark yield on the horizontal axis.

Interpretation of the diagram:

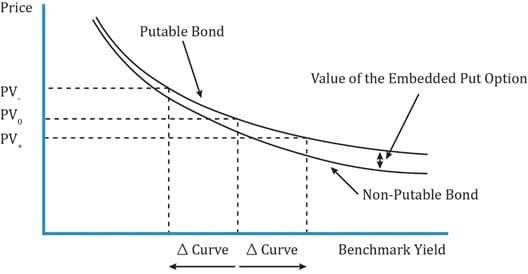

Interest Rate Risk Characteristics of Putable Bond

Interest Rate Risk Characteristics of Putable Bond

Source: CFA Program Curriculum, Understanding Fixed-Income Risk and Return

Interpretation of the diagram:

In the previous section, we saw how to calculate the duration for an individual bond. What if a portfolio consists of a number of bonds, how will its duration be calculated?

There are two ways to calculate the duration of a bond portfolio:

The key points related to each method are outlined in the table below.

| Weighted Average Time to Receipt of Aggregate Cash Flows | Weighted Average of Individual Bond Durations in Portfolio |

| Theoretically correct, but difficult to use in practice. | Commonly used in practice. |

| Cash flow yield not commonly used. Cash flow yield is the IRR on a series of cash flows. | Easy to use as a measure of interest rate risk. |

| Amount and timing of cash flows might not be known because some of these bonds may be MBS, or with call options. | More accurate as difference in YTMs of bonds in portfolio become smaller. |

| Interest rate risk is usually expressed as a change in benchmark interest rates, not as a change in the cash flow yield. | Assumes parallel shifts in the yield curve, i.e., all rates change by the same amount in the same direction. That seldom happens in reality. |

| Change in the cash flow yield is not necessarily the same amount as the change in yields to maturity on the individual bonds. |

Example 12: Calculating portfolio duration

An investment fund owns the following portfolio of three fixed-rate government bonds:

| Bond A | Bond B | Bond C | |

| Par value | 15,000,000 | 20,000,000 | 40,000,000 |

| Market value | 14,769,542 | 25,650,379 | 43,796,854 |

| Modified duration | 4.328 | 5.643 | 7.210 |

The total market value of the portfolio is 84,216,775. Each bond is on a coupon date so that there is no accrued interest. The market values are the full prices given the par value.

Solution to 1:

The average modified duration of the portfolio is 6.23.

(14,769,542/84,216,775) × 4.328 + (25,650,379/84,216,775) × 5.643 + (43,796,854/84,216,775) × 7.210 = 6.23.

Solution to 2:

The estimated decline in market value if each yield rises by 10 bps is 0.623%. -6.23 × 0.001 = -0.00623.

Ace the Exam with IFT Notes!

Ace the Exam with Active Learning!

Do IFT Mocks to make you exam-ready!

Do IFT Mocks to make you exam-ready!

Practice your way to success!

Accelerate your studies!

Sign up to get more!