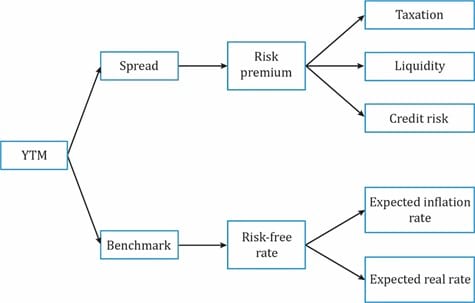

The yield spread is the difference in yield between a fixed-income security and a benchmark. Say the YTM of a 3-year corporate bond is 7.00%. The benchmark rate is 3-year Libor, which is 5.00%. The yield spread of the corporate bond relative to the benchmark is 2.00%. Generally, the benchmark reflects macroeconomic factors. A spread reflects microeconomic factors and aspects specific to the issuer, such as credit quality of the issuer and bond, tax status etc.

The YTM of a bond can be broken down into the following components:

Two related concepts are the G-spread and the I-spread.

The Z-spread (zero-volatility spread) is based on the entire benchmark spot curve. It is the constant spread that is added to each spot rate such that the present value of the cash flows matches the price of the bond. The Z-spread is also called the static spread as it is constant for all periods.

The option-adjusted spread (OAS) is the Z-spread adjusted for the value of an embedded option. Consider a callable bond with a Z-spread of 90 basis points, of which 10 basis points are due to the embedded call option. In this case, the OAS is 90 – 10 = 80 basis points. If a putable bond has a Z-spread of 180 basis points and the value of the put option is 10 basis points, the OAS is 180 + 10 = 190 basis points. Based on these simple scenarios, it should be clear that for a callable bond the OAS is lower than the Z-spread and for a putable bond, the OAS is higher than the Z-spread.

Example

A 5% annual coupon corporate bond with 3 years remaining to maturity is trading at 100.175. The 3-year, 3% annual payment government benchmark bond is trading at 100.50. The 1-year and 2-year government spot rates are 2.05% and 3.425% respectively. Calculate the G-spread, the spread between the yields-to-maturity on the corporate bond and the government bond having the same maturity.

Solution:

Solve for the yield-to-maturity on the corporate bond using the following keystrokes:

PV = -100.175, PMT = 5, FV = 100, N = 3, CPT I/Y = 4.936

The yield-to-maturity for the corporate bond is 4.936%.

The yield-to-maturity of the government bond can be calculated with the following keystrokes:

PV = -100.50, PMT = 3, FV = 100, N = 3, CPT I/Y = 2.824

The G-spread is 4.936% – 2.824% = 2.11% or 211 bps.

Ace the Exam with Active Learning!

Ace the Exam with IFT Notes!

Accelerate your studies!

Do IFT Mocks to make you exam-ready!

Do IFT Mocks to make you exam-ready!

Practice your way to success!

Sign up to get more!