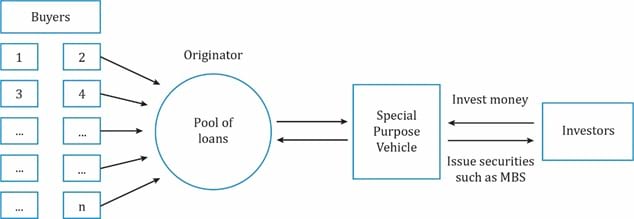

Asset-backed securities (ABS) are based on a principle called securitization. The securitization process involves pooling relatively straightforward debt obligations, such as loans or bonds, and using the cash flows from the pool of debt obligations to pay off the bonds created in the securitization process. The instruments which become part of the pool are called securitized assets. A simple securitization process is illustrated in the figure below:

In this illustration, a mortgage bank sells mortgage loans to thousands of homeowners. The mortgage bank bundles the individual loans into a pool which is sold to a separate legal entity generally referred to as a special purpose vehicle (SPV). The special purpose vehicle issues bonds to investors. The collateral for the bonds is the pool of mortgage loans.

The term mortgage-backed security (MBS) is commonly used for securities which are backed by high quality real estate mortgages. The term “asset-backed securities,” or ABS, is a broader concept that refers to securities backed by other types of assets. In the example above, we can say that the SPV issues MBS.

In this section, we look at the benefits from the perspective of the three parties involved in the securitization process: borrowers who are the homeowners, investors who want to buy mortgages, and the intermediary connecting these two parties which is a commercial bank/financial institution. Investors cannot lend directly to homeowners because they may be willing to lend/invest only a small amount of money, say $10,000, whereas the homeowner may require $100,000 as a mortgage loan. Second, the investor may not have all the information needed to assess the risk of the property.

Benefits to investors are as follows:

Benefits to the bank or loan originator are as follows:

Benefits to the borrowers of the loan are as follows:

We look at the securitization process in detail in this section.

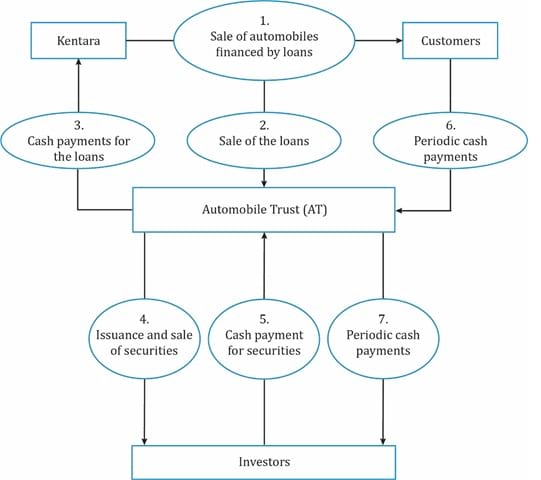

Kentara is a manufacturer of automobiles that range from $20,000 to $200,000. The majority of sales are made through loans granted by the company to its customers, and the automobiles serves as collateral for the loans. These loans, which represent an asset to Kentara, have maturities of five years, carry a fixed interest rate and are fully amortizing with monthly payments. Although the servicer of such loans need not be the originator of the loans, the assumption is that Kentara is the servicer.

Steps in the securitization transaction:

The exhibit below illustrates the steps involved in the securitization transaction for Kentara:

Source: Adapted from CFA Program Curriculum, Introduction to Asset-Backed Securities

Let us look at the parties involved in a securitization transaction.

| Party | Role | Party in our example |

| Seller of pool of securities | Originates the loans and sells to a special purpose entity (SPE). | Kentara |

| SPE or trust or issuer | Buys the loans from the seller and issues ABS. | Automobile Trust (AT) |

| Servicer | Services loans such as collecting payments from borrowers, notifying borrowers who may be delinquent and, if necessary, seizing automobiles from borrowers who do not make payments on time. | Kentara |

Note that a third party or the issuer may act as a servicer.

Other parties involved include independent accountants, underwriters, trustees, rating agencies, and guarantors.

Trustee: Safeguards the assets placed in the trust, and hold funds to be paid to bondholders.

In the Kentara example, assume 100,000 securities of Bond Class A were issued with a par value of $1,000 per security to raise $100 million. All the certificate holders in this case are treated equal because there is just one class of bondholders and there is no distinction between bondholders with respect to payment time or credit risk.

However, in reality not all bond issues are created with a similar structure. The motivation for the creation of different types of structures is to redistribute prepayment risk and credit risk efficiently among different bond classes in the securitization.

Prepayment risk is the uncertainty that the actual cash flows will be different from the scheduled cash flows, as set forth in the loan agreements, because borrowers may alter payments to take advantage of interest rate movements.

Instructor’s Note

Prepayment risk cannot be eliminated, but can be redistributed.

In the Kentara example, assume the buyers of automobiles are scheduled to make monthly payments towards the loan over 5 years. Instead, they prepay it in two years, perhaps because the interest rates decline, or due to any other reason. Since the loan is prepaid quicker than planned, the investors of ABS will also be paid quickly thereby reducing their interest income.

Time tranching: Creation of bond classes to distribute the prepayment risk is called time tranching. Cash flow received from customers is distributed among the tranches based on certain parameters. For example, assume AT issued the following four bond classes, with a total par value of $100 million, instead of one bond class:

Since the motive is to distribute prepayment risk, the A1 class may have a lower prepayment risk than A4. If customers prepay, then A4 bond-holders will get prepaid before A1.

Subordination and credit tranching: Subordination is another layering structure in securitization. The bond classes differ in their exposure to credit risk, i.e., how they share losses if the borrowers of the original loans default. An ABS is made up of a pool of loans. So, any default in payment will have a cascading effect on the investors. Here, several tranches of senior and subordinated classes are created and the credit risk is distributed to each class in a disproportionate manner based on the investor’s choice.

| Bond class | Par Value ($ millions) |

| A (senior) | 80 |

| B (subordinated) | 14 |

| C (subordinated) | 6 |

| Total | 100 |

In this example, all the losses are first absorbed by class C, then class B, and then class A. However, class C can accept a loss of up to $6 million. Beyond that, it is absorbed by class B. The risk is highest for class C and lowest for class A, in this example. Based on the high risk high return rule, the expected return of class C bondholders will be higher than that of class A bondholders.

The securitization of a company’s assets may include some bond classes that have better credit ratings than the company itself or its corporate bonds. Thus, in the aggregate, the company’s funding cost is often lower when raising funds through securitization than by issuing corporate bonds.

To understand why the funding cost is lower, we will go back to the Kentara example and consider two scenarios for raising $100 million: one in which Kentara issues a corporate bond, and another in which it issues ABS by securitizing loans/receivable.

Corporate bond scenario: Kentara issues corporate bonds for $100 million with auto loans as collateral. Assume credit-rating agencies such as Moody’s assign Kentara a credit-rating of BB (below investment-grade). The corporate bond rating will also be based on the company’s credit rating as it reflects the creditworthiness of debt securities. Kentara’s credit spread depends on the following two factors:

The cost of funding for Kentara will be higher if it issues a corporate bond, and not an ABS, for the following reasons:

Securitization Scenario

Ace the Exam with IFT Notes!

Ace the Exam with Active Learning!

Accelerate your studies!

Practice your way to success!

Do IFT Mocks to make you exam-ready!

Do IFT Mocks to make you exam-ready!

Sign up to get more!