Before discussing yield measures for money market instruments, it is important to understand the concept of periodicity. Periodicity is the number of compounding periods in a year, or number of coupon payments made in a year.

The stated annual rate for a bond will depend on the periodicity we are assuming. The stated annual rate is also called the annual percentage rate or APR.

Instructor’s Note

A quarterly coupon paying bond has a periodicity of four, while a semi-annual bond has a periodicity of two, and a monthly-pay bond with a given annual yield would have a periodicity of twelve.

“Compounding more frequently within the year results in a lower (more negative) yield-to-maturity.”

Consider a 5-year, zero-coupon bond priced at 80 per 100 par value. What is the stated annual rate for periodicity = 4, periodicity = 2, and periodicity = 1?

When periodicity = 4: compounding happens four times a year. N = 20; (5 years x 4 = 20). PMT = 0 as it is a zero-coupon bond. PV = -80; FV = 100; CPT I/Y = 1.12. This is the rate for each quarter. The stated annual rate is 1.12 x 4 = 4.487%.

When periodicity = 2: N = 10; PV = -80; PMT = 0; FV= 100; CPT I/Y = 2.2565. The stated annual rate is 2.25 x 2 = 4.51%.

When periodicity = 1: N = 5; PV = -80; PMT = 0; FV= 100; CPT I/Y = 4.56%. With a periodicity of 1, the stated annual rate is the same as the effective annual rate.

The formula for conversion based on periodicity is

Example

A 4-year, 3.75% semi-annual coupon payment government bond is priced at 97.5. Calculate the annual yield to maturity stated on a semi-annual bond basis and convert the annual yield to:

Solution to 1:

The stated annual yield to maturity on a semiannual bond basis can be calculated using a financial calculator: N = 8; PMT = 1.875; FV = 100; PV = -97.5; CPT I/Y. I/Y = 2.2195%. Hence, the stated annual yield to maturity = 2.2195% x 2 = 4.439%.

=

=

= 4.415%

= 4.415%

The annual rate of 4.439% for compounding semiannually compares with 4.415% for compounding quarterly.

Solution to 2:

= 4.488%

= 4.488%

The annual percentage rate of 4.439% for compounding semiannually compares with an effective annual rate of 4.488%.

The effective annual rate (EAR) is the yield on an investment in one year taking into account the effects of compounding. This rate has a periodicity of one as there is only one compounding period per year. EAR is used to compare the rate of return on investments with different frequency of compounding (periodicities).

Semiannual bond equivalent yield: Yield per semi-annual period times two. If the yield per semi-annual period is 2%, then the semi-annual bond equivalent yield is 4%.

Example

An analyst observes the following statistics for two bonds:

| Bond A | Bond B | |

| Annual Coupon Rate | 6.00% | 10.00% |

| Coupon Payment Frequency | Semi-annually | Quarterly |

| Years to Maturity | 4 years | 4 years |

| Price (per 100 par value) | 95 | 110 |

| Current Yield | ? | ? |

| Yield to Maturity | ? | ? |

Solution to 1:

The current yield for Bond A is 6/95 = 6.316% and the yield to maturity for Bond A is 7.469%.

The current yield for Bond B is 10/110 = 9.091% and the yield to maturity for Bond B is 7.106%.

Solution to 2:

Compare the yields for the same periodicity to answer this question. 7.106% for a periodicity of four converts to 7.169% for a periodicity of two. The additional compensation for the greater risk in Bond A is 30 bps (0.07469 – 0.07169).

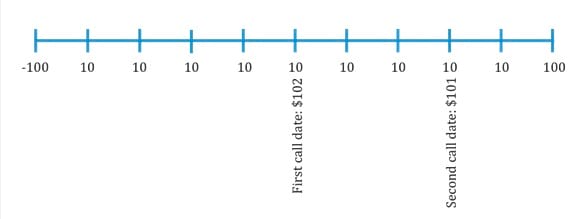

Example

Consider a bond which is selling for $100 and has the following cash flows:

Calculate the yield-to-first call and yield-to-second call.

Solution:

The yield-to-first call can be calculated as follows: PV= -100; N = 5; PMT = 10; FV = 102; CPT I/Y; I/Y = 10.325%. YTFC = 10.325%.

The yield-to-second call in our example will be 10.09%: PV= -100; N = 8; PMT = 10; FV = 101; CPT I/Y; I/Y = 10.09%.

Example

A bond with 4 years remaining until maturity is currently trading for 101.75 per 100 of par value. The bond offers a 5% coupon rate with interest paid semiannually. The bond is first callable in 2 years and is callable after that date on coupon dates according to the following schedule:

| End of Year | Call Price |

| 2 | 102.50 |

| 3 | 101.50 |

| 4 | 100.00 |

Solution to 1:

The yield-to-first-call can be calculated with the following key strokes:

PV = -101.75, FV = 102.5, N = 4, PMT = 2.5, CPT I/Y = 2.6342.

To arrive at the annualized yield-to-first-call, the semiannual rate must be multiplied by two. (2.6342 × 2 = 5.2684)

Solution to 2:

The yield-to-worst is 4.52%. The bond’s yield to worst is the lowest of the sequence of yields-to-call and the yield to maturity. Yield-to-first-call = 5.27%, Yield-to-second-call = 4.84%, and Yield to maturity = 4.52%.

Ace the Exam with IFT Notes!

Ace the Exam with Active Learning!

Do IFT Mocks to make you exam-ready!

Do IFT Mocks to make you exam-ready!

Practice your way to success!

Accelerate your studies!

Sign up to get more!