The money duration of a bond is a measure of the price change in units of the currency in which the bond is denominated, given a change in annual yield to maturity.

Money Duration = AnnModDur x PVFULL

ΔPVFULL≈ -MoneyDur x Δyield

Consider a bond with a par value of $100 million. The current yield to maturity (YTM) is 5% and the full price is $102 per $100 par value. The annual modified duration of this bond is 3. the money duration can be calculated as the annual modified duration (3) multiplied by the full price ($102 million): 3 x $102 million = $306 million. If the YTM rises by 1% (100 bps) from 5% to 6% the decrease in value will be approximately $306 million x 1% = $3.06 million. If the YTM rises by 0.1% (10 bps), the decrease in value will be $306 million x 0.1% = $0.306 million.

An important measure which is related to money duration is the price value of a basis point (PVBP). The PVBP is an estimate of the change in the full price given a 1 bp change in the yield-to-maturity. The formal equation is given below.

where PV_ and PV+ are full prices calculated by decreasing and increasing the YTM by 1 basis point.

A quick way of calculating the price value of a basis point is to take the money duration and multiply by 0.0001. For example, if the money duration of a portfolio is $200,000 the price value of a basis point is $200,000 x 0.0001 = $20. (1 bp = 0.01% = 0.0001)

Example 13: Calculating money duration of a bond

A life insurance company holds a USD 1 million (par value) position in a bond that has a modified duration of 6.38. The full price of the bond is 102.32 per 100 of face value.

Solution:

Example 14: Calculating PVBP for a bond

Consider a $100, five-year bond that pays coupons at a rate of 10% semi-annually. The YTM is 10% and it is priced at par. The modified duration of the bond is 3.81. Calculate the PVBP for the bond.

Solution:

Money duration = $100 x 3.81 = $381.00

PVBP = $381 x 0.0001 = $0.0381

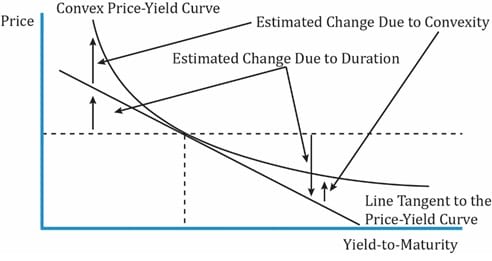

The graph below shows the relationship between bond price and YTM. It shows the convexity for a traditional fixed-rate bond.

Source: CFA Program Curriculum, Understanding Fixed-Income Risk and Return

Interpretation of the diagram:

Here we need to factor in the convexity. The percentage change in the bond’s full price with convexity-adjustment is given by the following equation:

Change in the price of a full bond:

![(-AnnModDur * \Delta yield) + [\frac{1}{2} * AnnConvexity * (\Delta yield)^2]](https://ift.world/wp-content/ql-cache/quicklatex.com-9ff30442c8ae7b3920920d1fff70516f_l3.png "Rendered by QuickLaTeX.com")

Expression in first braces: duration adjustment

Expression in second braces: convexity adjustment

Approximate convexity can be calculated using this formula:

where:

PV_ and PV+ = new full price when YTM is decreased and increased by the same amount

PV0 = original full price

The change in the full price of the bond in units of currency given a change in YTM can be calculated using this formula:

![\Delta PV_{FULL} \approx -(MoneyDur \times \Delta yield) + [\frac{1}{2} \times MoneyCon \times (\Delta yield)^2]](https://ift.world/wp-content/ql-cache/quicklatex.com-0a363a1f849420fa04e9ef6cce7acbbb_l3.png "Rendered by QuickLaTeX.com")

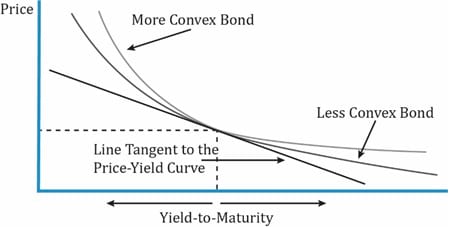

Convexity is good

The following exhibit shows the price-yield curves for two bonds with the same YTM, price, and modified duration, and why greater convexity is good for an investor.

Interpretation of the diagram:

The relationship between various bond parameters with convexity is the same as with duration.

For a fixed-rate bond,

Effective Convexity

For bonds whose cash flows were unpredictable, we used effective duration as a measure of interest rate risk. Similarly, we use effective convexity to measure the change in price for a change in benchmark yield curve for securities with uncertain cash flows. The effective convexity of a bond is a curve convexity statistic that measures the secondary effect of a change in a benchmark yield curve. It is used for bonds with embedded options.

Effective Convexity =

Here is a summary of some important points related to bonds with embedded options:

Example 15: Calculating the full price and convexity-adjusted percentage price change of a bond

A German bank holds a large position in a 6.50% annual coupon payment corporate bond that matures on 4 April 2029. The bond’s yield to maturity is 6.74% for settlement on 27 June 2014, stated as an effective annual rate. That settlement date is 83 days into the 360-day year using the 30/360 method of counting days.

Solution:

There are 15 years from the beginning of the current period on 4 April 2014 to maturity on 4 April 2029.

1. The full price of the bond is 99.2592 per 100 of par value.

FV = 100, I/Y = 6.74, PMT = 6.50, N = 15, CPT PV; PV = -97.777.

= 99.2592.

= 99.2592.2. PV+ = 99.1689

FV = 100, PMT = 6.5, I/Y = 6.75, N = 15, CPT PV; PV = -97.687.

= 99.1689.

= 99.1689.PV_ = 99.3497.

FV = 100, I/Y = 6.73, PMT = 6.5, N = 15, CPT PV; PV = -97.869.

= 99.3497.

= 99.3497. = 9.1075.

= 9.1075.The approximate modified duration is 9.1075.

= 201.493

= 201.493The approximate convexity is 201.493.

3. The convexity-adjusted percentage price drop resulting from a 100 bp increase in the yield-to-maturity is estimated to be -8.1% (-9.1075 + 1.00746).<

Modified duration alone estimates the percentage drop to be 9.1075%. The convexity adjustment adds 100.746 bps (0.5 × 201.493 × .012 = 1.00746%).

4. The new full price if the yield-to-maturity goes from 6.74% to 7.74% on that settlement date is 90.7623. The actual percentage change in the bond price is -8.5603%. The convexity-adjusted estimate is -8.1%.

Example 16: Calculating the approximate modified duration and approximate convexity

The investment manager for a US defined-benefit pension scheme is considering two bonds about to be issued by a large life insurance company. The first is a 25-year, 5% semiannual coupon payment bond. The second is a 75-year, 5% semiannual coupon payment bond. Both bonds are expected to trade at par value at issuance.

Calculate the approximate modified duration and approximate convexity for each bond using a 5 bp increase and decrease in the annual yield-to-maturity.

Solution:

In the calculations, the yield per semiannual period goes up by 2.5 bps to 2.525% and down by 2.5 bps to 2.475%.

The 25-year bond has an approximate modified duration of 14.18.

PV+ : FV = 100, I/Y = 2.525, PMT = 2.5, N = 50, CPT PV, PV = -99.2945.

PV– : FV = 100, I/Y = 2.475, PMT = 2.5, N = 50, CPT PV, PV = -100.7126.

= 14.18 and an approximate convexity of 284.

= 14.18 and an approximate convexity of 284. = 284.

= 284.Similarly, the 75-year bond has an approximate modified duration of 19.51 and an approximate convexity of 708.

Ace the Exam with IFT Notes!

Ace the Exam with Active Learning!

Accelerate your studies!

Do IFT Mocks to make you exam-ready!

Do IFT Mocks to make you exam-ready!

Practice your way to success!

Sign up to get more!