Financial analysis is the process of examining a company’s performance. For this purpose, financial reports are one of the most important sources of information available to a financial analyst. A financial analyst must have a strong understanding of the information provided in a company’s financial reports, notes, and supplementary information.

In order to understand financial analysis, we first need to understand the difference between the roles of financial reporting and financial statement analysis.

Financial reporting

The role of financial reporting is to provide information about a company’s performance (income statement and cash flow statement), financial position (balance sheet) and changes in financial position (statement of changes in equity).

Financial statement analysis

The role of financial statement analysis is to use the financial reports prepared by firms and combine them with other sources of information to decide if you can invest in the equity of the firm or lend money to the firm.

Instructor’s Note:

The financial statements mentioned below will be covered in a lot more detail in later readings. At this stage, you simply need to understand the basics.

The primary financial statements are the balance sheet, the income statement, the cash flow statement, and the statement of changes in owners’ equity.

Balance Sheet (Statement of Financial Position)

The balance sheet reports the firm’s financial position at a specific point in time. It has the following elements:

The relationship between the elements can be shown as:

Assets = Liabilities + Owners’ equity

The capital structure of a company represents the combination of liabilities and equity used to finance its assets. Both financial position and capital structure are useful in credit analysis.

Income statement

The income statement reports the financial performance of the firm over a period of time. It has the following elements:

The relationship between the elements can be shown as:

Net income = Revenues – Expenses

Cash flow statement

The cash flow statement reports the sources and uses of cash for the firm over a period of time. It has the following elements:

Statement of changes in owner’s equity

It reports the changes in the owners’ investment in the firm over time. It has the following elements:

Along with these required financial statements (mentioned above), a company typically provides additional information in its financial reports. This includes footnotes, management’s commentary, and auditor’s report.

Footnotes

They provide additional details about the information presented in financial statements. This includes important information about the accounting methods, estimates, and assumptions. They also contain information regarding acquisitions and disposals, commitments and contingencies, legal proceedings, employee stock options and other benefits, related party transactions and business, and geographic segments.

Management’s commentary

It provides an assessment of the data reported in the financial statements from the management’s perspective. Examples of content include trends and significant events affecting the company’s operations, liquidity and capital resources, off-balance sheet obligations, and planned capital expenditures.

Auditor’s report

An audit is an independent review of a firm’s financial statements. It enables the auditor to express an opinion on the fairness and reliability of the financial reports. An audit report can contain one of the following opinions:

For listed companies, the audit report also includes a discussion of Key Audit Matters (international) and Critical Audit Matters (US). Key Audit Matters and Critical Audit Matters include issues having a higher risk of misstatement, involving significant management judgment and estimates.

Other information sources

Apart from the above-mentioned sources, other information sources available for an analyst are:

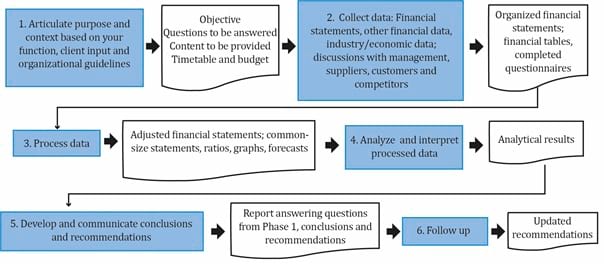

A financial statement analysis framework recommended by the CFA Institute is summarized in the figure below. The grey boxes represent phases of financial analysis while the white boxes represent outputs from each phase.

Articulate the Purpose and Context of Analysis

In this step we understand the purpose of the analysis. For example, an equity analyst analyzes the financial reports in order to decide whether to invest in the stocks of the company or not. On the other hand, a credit analyst looks at the company in a very different light, in order to judge whether it should be given a loan or not.

Next, the analyst defines the context which includes details such as the intended audience, time frame, budget and so on. Once the purpose and the context are defined, the analyst compiles the specific questions to be answered by the analysis, decides on the content to be prepared and finalizes the timeline and the budget.

Collect Data

Next, the analyst collects data required to answer the questions compiled in the previous step. The sources of data are financial reports and other information sources.

The output from this step includes: organized financial statements, financial tables and completed questionnaires.

Process Data

After collecting data, the analyst processes the data using appropriate analytical tools. This involves:

The output from this step includes: adjusted financial statements, common size statements, ratios, graphs and forecasts.

Analyze/Interpret the Processed Data

The next step is to interpret the processed data and come up with a decision. For example, an equity analyst may come up with a buy, sell or hold decision.

Develop and Communicate Conclusions/Recommendations

Next, the analyst communicates the conclusions or recommendations in the appropriate format. For example, an equity analyst will prepare a research report and send it to his firm’s clients.

Follow-up

Conduct periodic reviews to check if the previous conclusions are still valid. Change the conclusions/recommendations when necessary. For example, an equity analyst may send quarterly updates on his initial buy, sell or hold recommendation.

Ace the Exam with IFT Notes!

Ace the Exam with Active Learning!

Practice your way to success!

Accelerate your studies!

Do IFT Mocks to make you exam-ready!

Do IFT Mocks to make you exam-ready!

Sign up to get more!

Watch the lecture video.

Watch the lecture video. Read the summary to review concepts.

Read the summary to review concepts. Check your learning by doing the Quiz.

Check your learning by doing the Quiz.