IFT Notes for Level I CFA® Program

LM08 Currency Exchange Rates

Part 5

7. Exchange Rate Regimes – Ideals and Historical Perspective

Every exchange rate is managed to some degree by central banks. The policy framework adopted by a central bank or the monetary authority to manage its currency relative to other currencies is called the exchange rate regime.

You may ask, why must the central bank intervene in the exchange rate? This is because high exchange rate volatility can affect investment decisions or affect how foreign investors perceive the investment climate (risky or stable) of a country.

Before we look at the different exchange rate regimes, let us understand what an ideal regime must have.

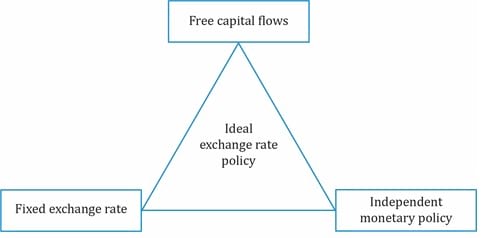

Properties of an ideal exchange rate regime:

- The exchange rate between any two currencies would be credibly fixed.

- All currencies would be fully convertible (i.e. currencies could be freely exchanged for any purpose and in any amount).

- Each country would be able to undertake fully independent monetary policy in pursuit of domestic objectives, such as growth and inflation targets.

But, in reality, these three properties are not consistent. If properties 1 and 2 hold good, then there would really be only one currency in the world and independent monetary policy will not be possible.

Historical perspective on currency regimes:

Note: This is not part of the learning objectives and there are no practice problems. However, a brief history of the currency regime is summarized below:

- Most of the 19th century until the start of World War 1 in 1914: the U.S. dollar and the U.K. pound sterling operated on the gold standard, meaning the price of each currency was fixed in terms of gold. Any other currency that fixed its price in terms of these two currencies was also indirectly operating on the gold standard. Trade imbalances, deflation, hyperinflation, economies facing depression paved way for a new standard instead of gold.

- Towards the end of World War II 1944 – early 1970s: A Fixed parity system called “The Bretton Woods” system was introduced by John Keynes and Harry White: adopted by 44 countries replacing the gold standard. There were now fixed parities for exchange rate between currencies. There would be periodic realignments of currencies to bring them back to the fixed parity or equilibrium state. Inflation issues, countries not able to exercise monetary policy, and excessive capital mobility made countries move to the floating exchange rate system.

8. A Taxonomy of Current Regimes

Exchange rate regimes for countries that do not have their own currency

Formal dollarization:

- Country uses the currency of another currency.

- The country cannot conduct its own monetary policy and imports the inflation of the country whose currency it uses.

- E.g. Panama uses the US dollar.

Monetary Union:

- Several countries use a common currency.

- Countries don’t have the ability to determine their own domestic monetary policy.

- E.g. European Union.

Exchange rate regimes for countries that have their own currency

Note: As we move down the exchange rate regimes in the below list, the currency volatility increases and the ability to implement independent monetary policy increases.

Currency board system:

- An explicit commitment to exchange domestic currency for a specified foreign currency at a fixed exchange rate.

- The country cannot conduct its own monetary policy and imports the inflation of the country whose currency it uses.

- E.g. Honk Kong issues HKD only when it is backed by equivalent USD holdings.

Fixed parity:

- A country pegs its currency within margins of ± 1% vs. another currency or basket of currencies.

- It is also called as conventional fixed peg arrangement.

- Exchange rate is maintained through:

- Direct intervention: Buying and selling foreign currency.

- Indirect intervention: Interest rate policies or regulating foreign transactions.

- E.g. Saudi Arabia uses a fixed parity with USD.

Target zone:

- Similar to a fixed parity, but with wider bands (± 2%).

- Authorities have more flexibility in monetary policies.

Crawling peg:

- Passive crawling peg: Allows for periodical adjustments in exchange rate, typically done to adjust for higher inflation versus the currency used in the peg.

- Active crawling peg: A series of adjustments are pre-announced and implemented over time making domestic inflation predictable.

- E.g. China.

Crawling bands:

- The width of bands used in fixed peg is increased over time to make the gradual transition from fixed parity to a floating rate.

Managed float:

- Monetary authority attempts to influence the exchange rate in response to specific indicators: balance of payments, inflation rates, or employment – without any specific target exchange rate.

Independently float:

- Exchange rate is entirely market-driven.

- Interventions are used only to reduce market fluctuations.

Share on :

Do IFT Mocks to make you exam-ready!

Do IFT Mocks to make you exam-ready!