As compared to households and corporations, the economic decisions made by governments can have an enormous impact on economies because governments are usually the largest employers, largest spenders and largest borrowers in an economy.

There are two types of government policy:

Monetary policy: Refers to central bank activities directed towards influencing the level of interest rates and money supply in the economy.

Fiscal policy: Refers to government decisions about taxation and spending.

The overall goal of these policies is to create an economic environment of stable growth and low inflation.

As stated above, monetary policy refers to central bank activities directed towards influencing the level of interest rates and money supply in the economy.

Money is generally defined as a medium of exchange. Instead of using the barter system to exchange goods and services, money facilitates an indirect exchange and helps overcome the drawbacks of a barter system.

For money to be a medium of exchange, it must:

Money fulfills three important functions. It:

Fractional reserve banking: Our modern banking system is known as fractional reserve banking because at any point in time, banks hold with them only a fraction of total deposits as reserves; this is based on the premise that not all customers want all of their money back at the same time.

Let us take the exhibit below (reproduced from the curriculum) to illustrate how fractional reserve banking results in money creation:

Money creation via Fractional Reserve Banking

| First Bank of Nations | |

| Assets | Liabilities |

| Reserves €10 | Deposits €100 |

| Loans €90 | |

| Second Bank of Nations | |

| Assets | Liabilities |

| Reserves €9 | Deposits €90 |

| Loans €81 | |

| Third Bank of Nations | |

| Assets | Liabilities |

| Reserves €8.1 | Deposits €81 |

| Loans €72.9 | |

Now let us go over the example. Assume the reserve requirement is 10%, that is, banks are required to retain only 10% of the total deposits as balances with them. The rest can be lent out.

First Bank of Nations: If a customer makes a deposit of €100, then the bank must retain €10 and the remaining €90 can be loaned out to another customer.

Second Bank of Nations: Now suppose, the person who receives this €90 loan from First Bank uses this money to purchase some goods of this value and the seller of the goods deposits €90 in another bank, the Second Bank of Nations. Again, the Second Bank must retain 10% of €90, which is €9, and may loan out the remaining €81 to another customer.

Third Bank of Nations: This customer in turn spends €81 on some goods and services. The recipient of this money deposits it at the Third Bank of Nations. Once again, the Third Bank must retain 10% of €81, which is €8.1, as part of its reserves and may loan out the remaining €72.9 to another customer.

This process continues until there is no more money to be deposited and loaned out. How much total money is created from an initial deposit of €100 in this process?, If you ask the first customer how much money he has, he will say €100, while the second customer will say €90, the third €72.9 and so on. It is the sum of all the deposits in the banking system. It can be calculated using this formula:

Amount of money created =

Money multiplier =

The money created in our example is  which is 1,000. Money multiplier is 10.

which is 1,000. Money multiplier is 10.

Example

Given a reserve requirement of 8 per cent, how much money can be created by depositing an additional $500?

Solution: C

The expression used to calculate the amount of money created is . Therefore,  = $6,250

= $6,250

Most economies distinguish money into two categories ‘Narrow money’ and ‘Broad money’.

Narrow money: Notes and coins in circulation plus other very highly liquid deposits.

Broad money: Narrow money plus the entire range of liquid assets used to make purchases.

Because financial systems, practice and institutions vary from economy to economy, so do the definitions of money.

The Quantity Theory of Money

We looked at this concept in a previous reading. Quantity theory of money states that total spending (in money terms) is proportional to the quantity of money.

M * V = P * Y

where:

M = quantity of money

V = velocity of circulation of money

P = average price level

Y = real output

If velocity is assumed to be constant as per quantity theory, then spending (P x Y) is proportional to the quantity of money (M).

Money neutrality

If money neutrality holds, then increasing money supply (M), and keeping the velocity (V) constant, will increase the price level (P) but real output (Y) will stay the same. In short, output cannot be increased by increasing the money supply. Money neutrality implies that an increase in money supply will ultimately lead to an increase in price level; real variables such as output and employment will not change in the long-run.

The amount of wealth that the citizens of an economy choose to hold in the form of money rather than in bonds or equities is known as the demand for money.

Motives for holding money:

Transaction-related

Precautionary

Speculative

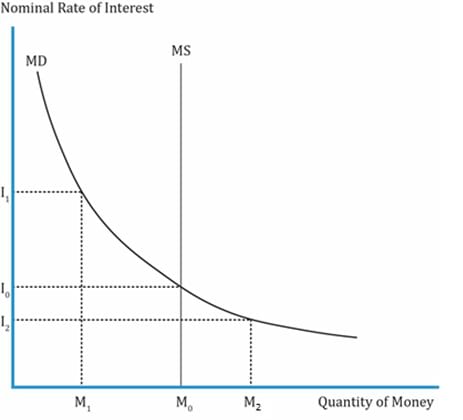

As with other markets, the price of money is determined by the interaction of demand and supply.

Interpretation of graph:

According to Fischer effect, the nominal interest rate is simply the sum of real interest rate and expected inflation.

Fischer Effect: Rnom = Rreal + πe

where:

Rnom = nominal interest rate

Rreal = real interest rate

πe = expected rate of inflation over any given time horizon

Fischer effect states that the real rate of interest in an economy is relatively stable and changes in nominal interest rates are due to changes in expected inflation. This is directly related to the concept of money neutrality.

But, investors can never be sure of how much inflation or real growth would be in the future. They, therefore require an additional return for bearing this risk, which is called the risk premium.

When we consider uncertainty, nominal interest rates have three components:

For example: Let us assume an investor invests in a corporate bond that offers a yield of 15% over the next year. It can be broken down into three components: real return of 4%, expected inflation of 8% and risk premium of 3%. (You will learn in ‘fixed income’ section that we can further divide this risk premium into credit risk premium, liquidity risk premium and so on.)

Ace the Exam with Active Learning!

Ace the Exam with IFT Notes!

Accelerate your studies!

Practice your way to success!

Do IFT Mocks to make you exam-ready!

Do IFT Mocks to make you exam-ready!

Sign up to get more!