IFT Notes for Level I CFA® Program

LM05 Monetary and Fiscal Policy

Part 2

4. Roles of Central Banks & Objectives of Monetary Policy

- Monopoly supplier of the currency: Central banks are the only authority with the capacity to print money.

- Banker to the government and the banker’s bank: Central banks provide banking services to the government and other banks in the economy.

- Lender of last resort: Because central banks have the capacity to print money, they are able to supply funds to banks that are facing a shortage and helps prevent a run on the bank.

- Regulator and supervisor of the payments system: Oversees, regulates and sets standards for a country’s payments system for millions of transactions that happen on a daily basis. It also coordinates with other central banks around the world to formulate processes.

- Conductor of monetary policy: Most important role of the central bank. It takes actions to control or influence the quantity of money and credit in an economy.

- Supervisor of the banking system: This varies from one country to another. But, in many countries, the central bank along with one/more regulatory authorities oversees the banking system including granting licenses for a new bank, etc.

- Manage foreign currency reserves and gold reserves: The central bank may decide to sell foreign currency from its reserves if its domestic currency is under sustained pressure and continues to depreciate quickly. For example, The Reserve Bank of India (RBI) repeatedly sold dollars in 2012 to boost the Indian rupee.

4.1 The Objectives of the Monetary Policy

Central banks normally have a variety of objectives (i.e. to maintain full employment and output, to maintain confidence in the financial system, or to promote understanding of the financial sector), but the overriding one is nearly always price stability or keeping inflation in check.

5. The Costs of Inflation

Expected inflation can give rise to:

- Menu costs: Due to high inflation, businesses constantly have to change the advertised prices of their goods and services. This is known as menu cost.

- Shoe leather costs: In times of high inflation, people would naturally tend to hold less cash and would therefore wear out their shoe leather in making frequent trips to the banks to withdraw cash. This is known as shoe leather cost. (However, in a modern economy, with internet banking and online transactions, the shoe leather costs are much lower as compared to the past)

If consumers/firms are aware of expected inflation, then they can negotiate wage increases or factor-in price rise in the goods and services ahead of time. But, in reality, all prices are not indexed to inflation and there is a surprise element in the form of unexpected inflation, the costs of which can be substantial.

Unanticipated (unexpected) inflation can, in addition:

- Lead to inequitable transfers of wealth between borrowers and lenders: If inflation is higher than expected, then borrowers benefit at the expense of lenders because the real value of borrowing declines. Similarly, if inflation is lower than expected, then lenders benefit at the expense of borrowers because the real value of the payment on debt increases. For example, if a government borrowed $100 million at a fixed rate and the expected inflation at the time of borrowing was 8%. But, during the life of this bond, assume the inflation increases to 15%. In nominal terms, the government will still repay $100 million, but because of the higher than expected inflation, investors will lose as it is worth less at the time of repayment. The government benefited from the increase in inflation.

- Give rise to risk premia in borrowing rates and the prices of other assets: Lenders will demand higher rates if there is high uncertainty in inflation; the borrowing costs for firms goes up which negatively impacts the economy.

- Reduce the information content of market prices: Information about supply and demand from changes in prices becomes less reliable.

6. Monetary policy tools

The three tools available to central banks to control the money supply are: open market operations, refinancing rates and reserve requirements.

-

6.1 Open market operations

- Increase or decrease the amount of money in circulation.

- Increase money supply by buying government bonds from commercial banks à this increases the reserves of private banks à lends this money to firms and households, which then multiplies.

- Decrease money supply by selling government bonds to commercial banks à this decreases private banks’ reserves to lend money to firms and households.

-

6.2 The Central Bank’s Policy Rate

- Official interest rate: Known by different names in different countries. Called the official interest rate, or official policy rate, or policy rate, or discount rate. The objective is to influence short- and long-term interest rates.

- Repo rates: The rate at which the central bank is willing to lend money to commercial banks. The way it achieves this policy-rate setting is through a repurchase agreement wherein the central bank sells a security to commercial banks with a commitment to repurchase after a certain number of days. The maturity varies from overnight to two weeks; these are short-term collateralized loans. The rate implicit in this agreement is called repo rates.

- Base rates: The name varies from economy to economy. This is the rate at which commercial banks are willing to lend to each other.

- Federal funds rate: This is specific to the U.S. It is the interbank lending rate on overnight borrowings of reserves.

- In general, if the policy rate is high, the amount of lending will decrease and the quantity of money will decrease. On the other hand, if the policy rate is low, then the amount of lending will increase and the quantity of money will increase.

6.3 Reserve Requirements

We looked at the reserve ratio briefly at the beginning of this reading in the ‘fractional reserve system’ topic. The central bank may change the money supply in the economy by changing the reserve requirement. If the reserve requirement is low, then the money multiplier (reciprocal of reserve requirement) goes up and the money supply increases. Similarly, if the reserve requirement is high, then the money multiplier goes down and the money supply decreases.

6.4 The Transmission Mechanism

We looked at the tools used by central banks to influence rates, in the previous section. Now, we will see how policy decisions (especially the policy rate) transmits across the economy and affects the price level. One of the notable points from the previous section was that the policy rates set by central banks are short-term in nature, ranging from overnight to a few weeks. So, how does it affect the economy (growth, employment) in the long run? This is because central bankers believe money neutrality does not hold in the short run. The effects are not often immediate across the economy when official interest rates rise; there is a lag.

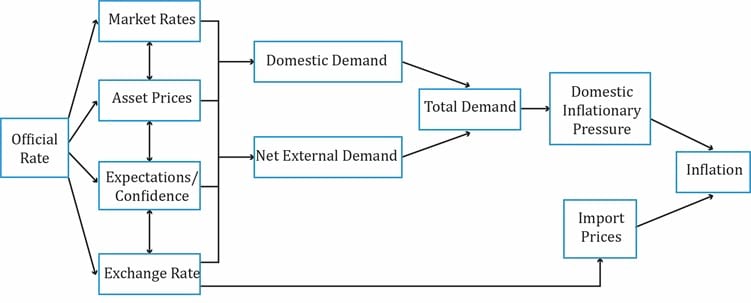

The exhibit below is reproduced from the curriculum:

A Styled Representation of the Monetary Transmission Mechanism

Interpretation of the exhibit:

For simplicity, let us break it down into three parts.

- Link between the changes in official rates on other related markets: To restrict money supply, the central bank may decide to increase official interest rates. This affects four interrelated channels:

- Market rates: An increase in official interest rates is reflected in short-term bank lending rates. Once the policy rate goes up, banks increase the base rates, which in turn affect the rates at which banks lend to customers (mortgages, loan rates). The rates on savings deposits also change, but not by the same amount as banks maintain a difference between deposit and loan rates.

- Asset prices: Market value of securities such as bonds and equities decreases when the official interest rates rise. In the case of bonds, prices are inversely related to long-term interest rates. Securities prices also decrease because future cash flows are discounted by a larger factor.

- Expectations/confidence: Increase in rates could influence (dent) expectations about the future prospects of the economy, such as employment opportunities, firms’ profitability, unemployment levels, etc. A rate increase may also imply the economy is growing faster than expected. Or, it could mean it is time to slow the growth in the economy and tame inflation, which would in turn lower confidence.

- Exchange rate: The exact impact is uncertain. But, an unexpected increase in official rate will lead to an appreciation of the domestic currency. A stronger domestic currency makes exports unattractive to overseas buyers as it is more expensive in their currency terms. This would lower the exporters’ profitability.

Impact on individuals/households: Discourages borrowing, reduces spending, postponing consumption.

- Discourages consumer spending. Individuals tend to postpone consumption and are more inclined to save, if rates increase.

- The tendency to borrow to consume will also be low because of higher rates and interest rate expectations. If further rate increases are anticipated, then consumers will not borrow.

- Disposable incomes of individuals decrease as prices increase.

- The fall in asset prices affects their financial wealth. Higher rates à mortgage rates higher à lower demand à fall in market prices of houses.

- The outflow for those with mortgages increases.

- Makes domestic goods expensive relative to foreign goods. There may be a tilt in spending with more being spent on imported goods.

Impact on firms: Depends on the cost of capital

- Higher borrowing costs.

- Reduced profitability.

- Deferred new projects, investment spending, and hiring plans.

- Impact on aggregate demand:

- Changes in consumption and investment spending behavior of consumers and firms affect aggregate demand. Low confidence à low spending à low demand.

- Increase in rate reduces real domestic demand and net external demand (difference between export and import consumption).

- Total aggregate demand goes weak.

- Impact on inflation:

- Determines the nominal value of goods and services in the long run.

- Weaker demand may put a downward pressure on inflation.

7. Inflation Targeting

Some economies implement monetary policy by targeting a certain level of inflation and then ensuring this level is met by monitoring a range of monetary and real economic indicators.

The success of inflation targeting depends on the following three factors that assess the effectiveness of a central bank:

| Central Bank Independence (free from political interference) |

The degree of independence varies across economies. Some are operationally and target-independent, i.e. they determine the level of inflation to target, how to meet that target, and by when it must be achieved. There are others where the bank is assigned a rate of inflation to target by the government. Here, the government determines the appropriate level of inflation. So, they are only operationally independent.

|

| Credibility |

Follows through on its stated policy intentions. Is the central bank independent and does the market/public have confidence in the policy measures? |

| Transparency |

Clear policy on economic indicators: Is the central bank transparent about its decision-making process? Being transparent in its quarterly assessment is one of the ways to gain credibility. What are the indicators the bank monitors before making the interest rate/policy decision? |

Other features of an inflation-targeting framework include:

- A decision-making framework that considers a wide range of economic and financial market indicators.

- A clear, symmetric, and forward-looking medium-term inflation target, sufficiently above 0 percent, to avoid the risk of deflation, but low enough to ensure a significant degree of price stability. Similarly, it should not be too high either, because a high rate would result in price instability and inflation volatility.

- Exhibit 9 in the curriculum lists inflation targets for several economies. They are usually between 2% and 3%. For instance, if a country sets the target to 0.5% and misses it, then it runs the risk of deflation (or negative inflation).

- The inflation target set by central banks can become self-fulfilling prophecies if economic agents believe the target will be met. Wage negotiations will factor in this level of inflation.

The following are some of the obstacles in successful implementation of monetary policy in developing economies:

- Rapid financial innovation.

- Absence of liquid government-bond market.

- Lack of independence of central banks.

- Rapidly changing economy.

- Poor track record in controlling inflation in the past.

8. Exchange Rate Targeting

Instead of targeting inflation, some economies implement monetary policy by targeting the exchange rate. It is done by setting a fixed level or band of values for the exchange rate against a major currency.

How it works:

- Government/central bank announces the target.

- Central bank supports the target by buying and selling the national currency in foreign exchange markets.

- “Import” the inflation experience of the low inflation economy.

- Interest rates and conditions in the domestic economy must adapt to accommodate this target and domestic interest rates and money supply can become more volatile.

- Let us take a simple example: The central bank of Brazil announces that it wishes to maintain a specific exchange rate against the U.S. dollar. Brazil, being a developing economy, faces volatile inflation. If inflation is higher than the U.S.’s, then its currency, the real, falls against the USD. To arrest its fall, Brazil’s central bank would sell dollar reserves and buy reals. It restricts the money supply and increases short-term interest rates. In contrast, if the inflation was low, and the real appreciates against the USD, then the central bank would have to buy USD and sell real. This explains how domestic interest rates and money supply can be volatile when targeting an exchange rate.

In a pegged exchange rate, a country fixes the value of its currency against either the value of another single currency, a basket of other currencies, or another measure of value, e.g. gold. In dollarization, a country uses US dollar as its functional currency.

What you cannot do because of exchange rate targeting:

- Monetary policy is not independent.

- Monetary policy cannot be used to target domestic inflation.

9. Monetary Policies: Contractionary, Expansionary, Limitations

Central banks control liquidity by adjusting policy rates.

Contractionary monetary policy:

- High economic growth leads to high inflation. To cool off the economy, a central bank may employ a contractionary monetary policy.

- The central bank does this by increasing the official policy rate. This restricts the growth rate of money supply and the real economy contracts.

Expansionary monetary policy:

- To boost a slowing economy, the central bank decreases the official policy rate. This increases liquidity and growth rate of money supply and the real economy expands.

- This is only in the short-run. Given the money neutrality theory, increasing or decreasing interest rates will not affect the real economy in the long-run.

High and low policy rate is with respect to the neutral rate of interest:

- It is the rate of interest that neither spurs nor slows the economy.

- Typically neutral rate = Trend growth rate in the long run + long run expected inflation

- If policy rate > neutral rate, then the monetary policy is contractionary.

- If policy rate < neutral rate, then the monetary policy is expansionary.

Neutral rate = trend growth rate + inflation target

In an economy, if the trend growth rate is 3% and inflation target is 2%, then the neutral rate will be 5%. If the policy rate is set above 5%, then we have a contractionary policy. If the policy rate is set below 5%, then we have an expansionary monetary policy.

9.1 What’s the Source of the Shock to the Inflation Rate?

The central bank must consider the source of inflation before deciding on contractionary/expansionary policy action. Two sources of shock to the inflation rate are:

- Demand shock: Caused by an increase in consumer confidence, which leads to more consumption and investment spending. Raising interest rates to control inflation is apt here.

- Supply shock: Caused by an increase in a supply factor such as oil prices. Raising interest rates is not appropriate as consumption will tend to fall, and consequently there will be an increase in unemployment.

9.2 Limitations of Monetary Policy

The will of the monetary authority does not necessarily transmit seamlessly through the economy.

This is because central banks cannot control:

- The amount of money households and corporations put in banks on deposits.

- The willingness of banks to create money by expanding credit.

It is relatively easy for central banks to influence short-term rates but long-term rates depend on expectations of interest rates and are not easy to control.

What is quantitative easing?

Quantitative easing is an unconventional monetary policy used when the traditional policy becomes ineffective. It is used to increase money supply where the central banks print (these days electronically) money to buy any assets.

Share on :

Do IFT Mocks to make you exam-ready!

Do IFT Mocks to make you exam-ready!