Factors of production are the inputs used by a firm to produce goods and services. These inputs include land, labor, capital, and raw materials. For simplicity, we will consider only two inputs:

Before moving on, let us understand a few basic terms.

Cost of production. The total cost of production is given by the equation below:

where:

w is the wage rate per hour

L is the number of labor hours

r is the cost per hour of capital and

K is number of hours for which capital is used.

Two factors that lower the cost of producing at a given level of output are:

Total Product, Average Product, and Marginal Product

Total product is the total output from all inputs during a time-period. It is denoted by TP or Q. Total product gives information about the total production of a firm during a time-period, but reveals very little about how efficient the firm is.

Average product is the total product divided by the quantity of a given input. It measures the productivity of an input. The average product of labor is given by:  or

or  .

.

Marginal product is the amount of additional output resulting from using one more unit of input, assuming other inputs are fixed. It is calculated by dividing the change in total product by the change in the quantity of input. Hence, the marginal product of labor is: or

or

Let us take an example of three companies X, Y and Z whose total product and average product of labor are given below:

| Company | Output (TP) | Labor hours | AP = TP/L |

| Company X | 250,000 | 250 | 1,000 |

| Company Y | 450,000 | 500 | 900 |

| Company Z | 500,000 | 625 | 800 |

It is not possible to identify the most efficient company by looking at just the TP values. AP is a better measure of efficiency. Company X has the highest AP and is therefore the most efficient.

The table below shows TP, AP and MP of labor for a firm across different levels of labor:

| Units of Labor (L) | TP | AP | MP |

| 1 | 100 | 100 | 100 |

| 2 | 210 | 105 | 110 |

| 3 | 300 | 100 | 90 |

| 4 | 360 | 90 | 60 |

| 5 | 400 | 80 | 40 |

| 6 | 420 | 70 | 20 |

| 7 | 350 | 50 | -70 |

Interpretation:

Economic profit is the difference between the total revenue and total economic costs. It is also known as abnormal profit. Another definition of profit is accounting profit. Accounting profit is the difference between the total revenue and total accounting costs.

Economic profit = Total revenue – Total economic costs

Economic profit = Accounting profit – Total implicit opportunity costs

Accounting profit = Total revenue – Total accounting costs

Economic cost considers opportunity costs, while accounting cost does not. Economic cost is the sum of accounting cost and opportunity cost. Let us take an example. Assume Megan starts a business with an equity capital of $100 million. The required return on the invested amount is 10%. Hence, the opportunity cost is 10% of $100 million = $10 million. If the accounting cost is $190 million, then the total economic cost is $200 million. Continuing with this example, if the revenue is $200 million, the economic profit is zero and the accounting profit is $10 million. In this case, it can be said that the business is earning a normal profit of $10 million.

Instructor’s Note:

In this reading, ‘cost’ refers to economic cost and ‘profit’ refers to ‘economic profit’.

If a firm’s revenue is equal to the firm’s total economic cost, the economic profit is zero and the firm is said to be earning a normal profit.

Accounting profit = economic profit + normal profit.

Normal profit = implicit costs or opportunity costs.

Marginal Revenue

Marginal revenue is defined as the change in total revenue divided by the change in quantity. It is the incremental revenue because of producing an additional unit per time-period. It is expressed as:

We will now analyze marginal revenue under two market conditions: perfect competition and imperfect competition.

Marginal revenue under perfect competition

In a perfectly competitive market:

Marginal revenue under imperfect competition

In an imperfect competitive market:

Marginal Cost

Marginal cost is the incremental cost of producing one more unit. It can be calculated by dividing the change in total cost by the change in quantity. It is expressed as:

Economists distinguish between short-run and long-run marginal cost. Short-run marginal cost is the cost of producing an additional unit assuming only labor costs vary and all other factors of production are constant. Short-run marginal cost is directly related to wage price and inversely related to productivity. Short-run marginal cost,  . Long-run marginal cost is the cost of producing one more unit assuming all factors of production are variable.

. Long-run marginal cost is the cost of producing one more unit assuming all factors of production are variable.

Fixed and Variable Costs

Total cost can be broken down into fixed and variable costs. Fixed costs do not change with the quantity of output. Variable costs change with the quantity of output. Average variable cost is the ratio of total variable cost to quantity. It is expressed as:

Profit Maximization

A firm’s profit is maximized at a level of output where marginal revenue is equal to marginal cost (MR = MC). If marginal revenue exceeds marginal cost, a firm can increase profits by producing more. If marginal revenue is less than marginal cost, the firm should scale back. This discussion assumes that marginal cost is rising with increased output.

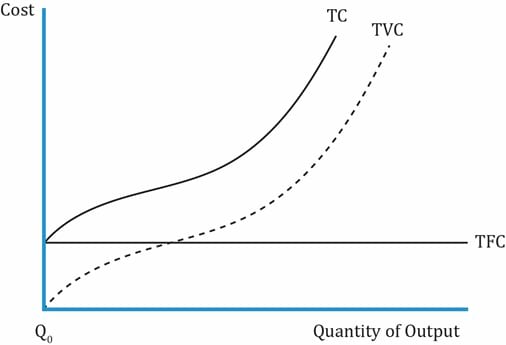

Understanding the Interaction between Total, Variable, Fixed, and Marginal Cost and Output

All the graphs we look at in this section are from a short-run perspective. In the short run, one or more factors of production are fixed. Usually capital is fixed in the short run while labor may change. The graph below shows the cost curves for a firm in the short run.

Interpretation of the graph:

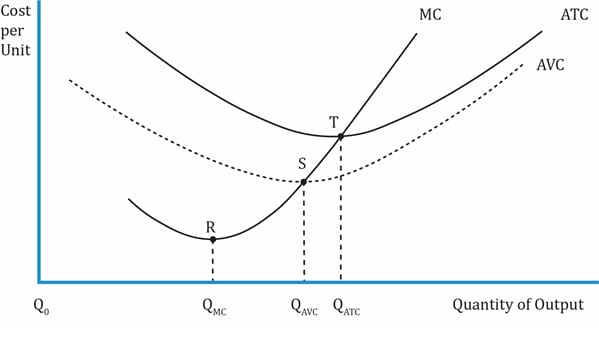

The graph below shows the MC, ATC and AVC curves for a firm in the short run.

Interpretation of the graph:

AVC Curve

ATC Curve

Marginal cost curve

AFC

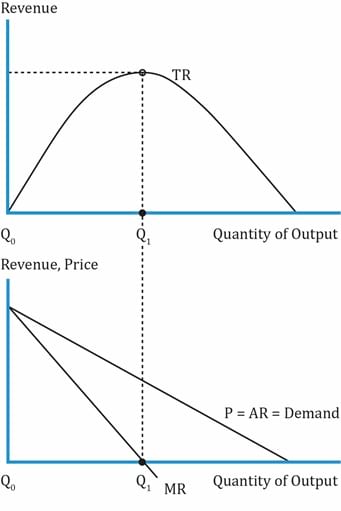

Revenue under Conditions of Perfect and Imperfect Competition

Total revenue under perfect competition:

Total revenue under imperfect competition

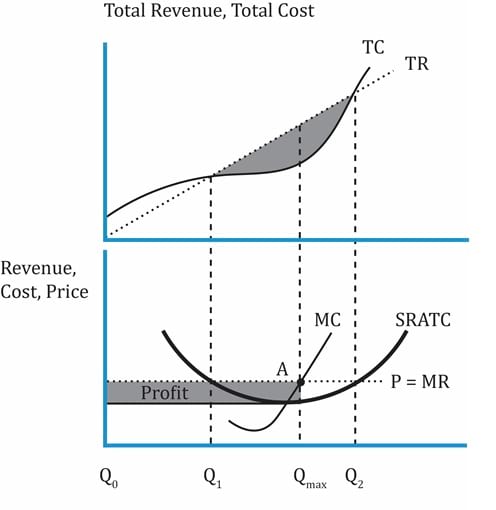

Profit Maximization, Breakeven, and Shutdown Points of Production

Profit is maximized when:

The graph below shows the TR, TC, demand curve, and profit maximization under perfect competition.

Qmax is the profit maximizing quantity where MR = MC and MC is rising.

Breakeven Analysis

A firm is said to breakeven under the following conditions:

When a firm is operating at its breakeven point, the economic profit is zero. It might still be earning a positive accounting profit.

A perfectly competitive market with no barriers to entry will attract new entrants. The increased competition will lead to increased output and lower prices in the long run where no firm is able to earn an excess return or positive economic profit.

Instructor’s Note

If economic profit is zero, accounting profit is called normal profit.

Under perfect competition, firms earn only normal profits in the long run.

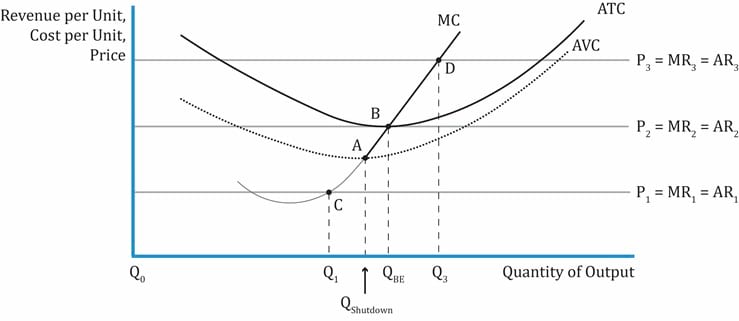

The Shutdown Decision

The relationships that show when a firm must operate or shutdown are given in the table below:

| Short-run effect of the relationship between price and ATC on a firm | ||

| Situation | Short run | Long run |

| Operate | Operate | |

| but TR < TC | Operate | Exit |

| TR < TVC | Shutdown | Exit |

Let us understand a firm’s breakeven and shutdown point using the graph below.

Interpretation of the graph:

Ace the Exam with IFT Notes!

Ace the Exam with Active Learning!

Accelerate your studies!

Do IFT Mocks to make you exam-ready!

Do IFT Mocks to make you exam-ready!

Practice your way to success!

Sign up to get more!