| Financial reporting quality | |

| Low | High |

| Low quality reports contain information that is pure fabrication. | High-quality reports contain information that is relevant, complete, neutral, and free from error. |

| Low financial reporting quality impedes assessment of earnings quality and impedes valuation. | High financial reporting quality enables assessment. |

| Earnings (results) quality | |

| Low | High |

| Low earnings quality is unsustainable. | High earnings quality increases company value.

High earnings quality is sustainable. |

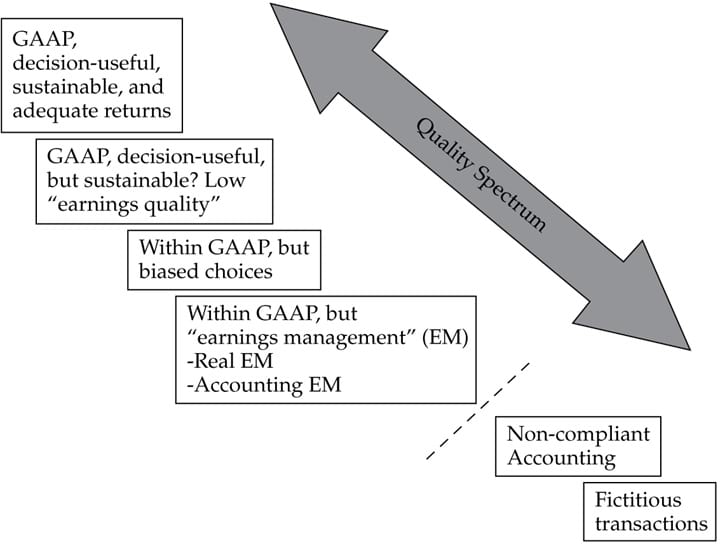

From an investor’s perspective, the overall quality of financial reports, that is combining reporting quality and earnings quality, can be thought of as a continuous spectrum ranging from highest to lowest as depicted in the diagram below:

Sign up to get more!