101 Concepts for the Level I Exam

Essential Concept 86: Private Equity Fund Structures, Terms, Valuation and due Diligence

![]()

Fund structure:

Most PE firms are structured as limited partnerships, where the fund manager is the general partner (GP) and the fund’s investors are limited partners (LP). The GP has management control over the fund and is jointly liable for all debts. The LPs have limited liability; they do not risk more than the amount of their investment in the fund.

Two core functions of the GP are: (1) to raise funds and (2) To manage investments

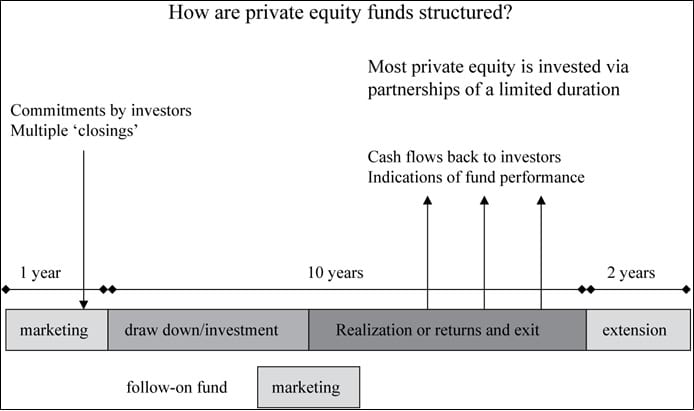

The following figure shows the funding stages for a private equity firm.

Terms:

The most significant economic terms are:

- Management fees: represent a percentage of committed capital paid annually to the GP.

- Transaction fees: fees paid to GPs in their advisory capacity when they provide investment banking services for a transaction.

- Carried interest: represents the general partner’s share of profits generated by a private equity fund.

- Ratchet: mechanism that determines the allocation of equity between shareholders and the management team of the portfolio company.

- Hurdle rate: the IRR that a private equity fund must achieve before the GP receives any carried interest.

- Target fund size: expressed as an absolute amount in the fund prospectus.

- Vintage year: the year the private equity fund was launched. Reference to vintage year allows performance comparison of funds of the same stage and industry focus.

- Term of the fund: typically 10 years, extendable for additional shorter periods (by agreement with the investors)

The most significant corporate governance terms are:

- Key man clause: If a key executive leaves, the GP is prohibited from making new investments until a new key executive is appointed.

- Disclosure and confidentiality: Private equity firms have no obligations to disclose publically their financial performance. Some terms limit the information available to investors.

- Clawback provision: If a fund makes profitable exits in early years, but the subsequent exits are less profitable, then the GP has to pay back profits to ensure that the profit split is in line with the fund prospectus. The two types of clawback provisions are-

- Due on termination

- Annual reconciliation (true-up)

- Distribution waterfall: Mechanism to ensure LPs are paid first before the GP receives carried interest. The two main types are:

- Deal-by-deal waterfall – Allowing distribution after each deal.

- Total return waterfall – Distribution is calculated on the entire portfolio.

- Tag-along, drag along rights: Any future acquirer has to extend acquisition offer to all shareholders, including the management of the company.

- No-fault divorce: A GP may be removed without cause, if a super majority of LPs approve that removal.

- Removal for “cause”: Allows removal of GP or early termination of fund for causes such as gross negligence, ‘key person’ event, felony conviction, bankruptcy, or material breach of the fund prospectus.

- Investment restrictions: Minimum level of geographic or sector diversification, or limits on borrowing.

- Co-investment: LPs have the first right of co-investing along with the GP if the GP launches a new fund.

Valuation:

The value of a fund is based on NAV. The fund’s assets are valued by GPs in the following ways:

- At cost with significant adjustments for subsequent financing events or deterioration.

- At lower of cost or market value.

- By a revaluation of a portfolio company whenever a new financing round involving new investors takes place.

- At cost with no interim adjustment until the exit.

- With a discount for restricted securities.

- More rarely, marked to market by reference to a peer group of public comparables and applying illiquidity discounts.

Due diligence:

Due diligence is important because:

- PE funds show strong persistence of returns over time. This means that top performing funds tend to continue to outperform and poor performing funds also tend to continue to perform poorly or disappear.

- Difference between performances of funds is extremely large. For example, the difference between top quartile and third quartile fund IRRs can be about 20 percentage points.

- Liquidity in private equity is low and LPs are locked for the long term. On the other hand, when private equity funds exit an investment, they return the cash to the investors immediately. Therefore, the “duration” of an investment in private equity is typically shorter than the maximum life of the fund.

Share on :