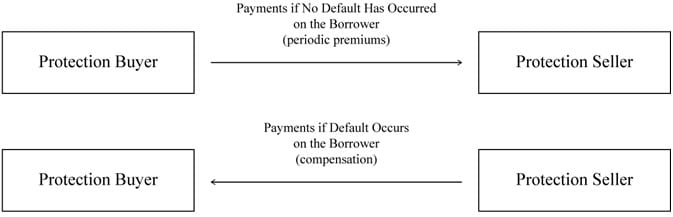

A credit default swap is a derivative contract between two parties, a credit protection buyer and credit protection seller, in which the buyer makes a series of cash payments to the seller and receives a promise of compensation for credit losses resulting from the default of a third party.

The figure below shows the structure of payment flows.

The ISDA master agreement is a document that lays down the rules that all CDS contracts must conform to and other guidelines for the functioning of the CDS market.

Each CDS contract has a notional amount and maturity date.

The debt of the third party on which the CDS is written, is called the reference entity. The CDS covers all issues of the reference entity with similar or higher seniority. The underlying is the credit quality of a borrower.

The payoff on the CDS is determined by the cheapest-to-deliver obligation, which is a debt instrument with the lowest cost but same seniority as the reference obligation.

There are three types of CDS:

Sign up to get more!