Effective duration indicates the sensitivity of a bond’s price to a 100-bps parallel shift of the benchmark yield curve in particular, the government par curve; assuming no change in the bond’s credit spread.

The flowing procedure is used to apply this formula in practice.

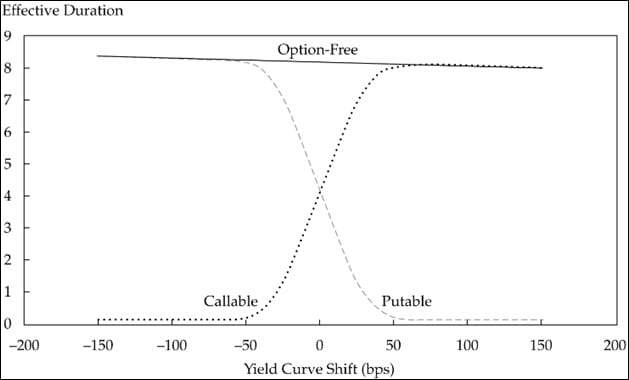

The following figure compares the effective duration of option-free, callable and putable bonds.

The effective durations of various types of instruments are shown in the table below.

| Type of Bond | Effective Duration |

| Cash | 0 |

| Zero-coupon bond | ≈ Maturity |

| Fixed-rate bond | < Maturity |

| Callable bond | ≤ Duration of straight bond |

| Putable bond | ≤ Duration of straight bond |

| Floater (Libor flat) | ≈ Time (in years) to next reset |

Sign up to get more!